Operational Realities of the Contemporary Nail Industry

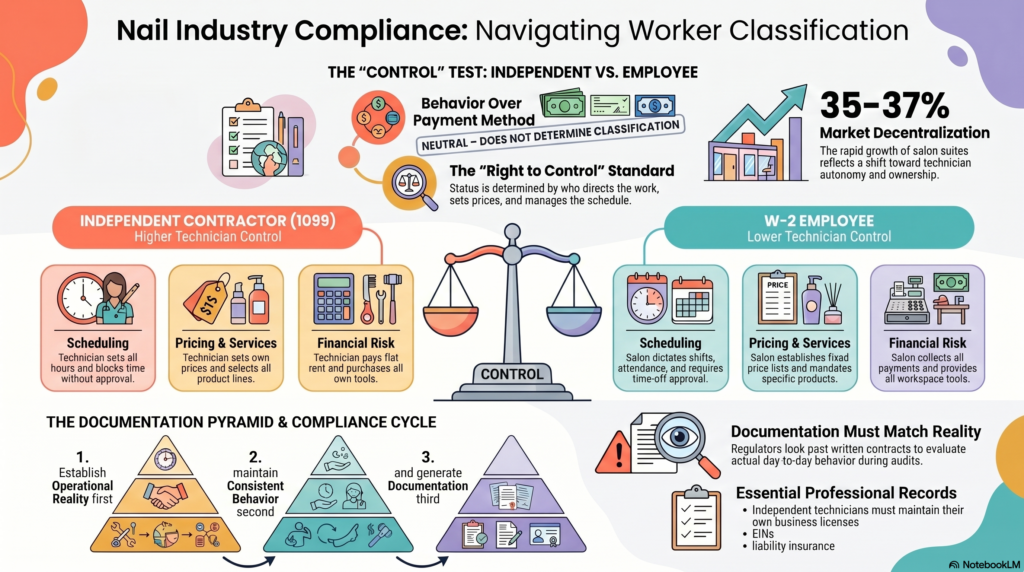

The modern beauty sector, particularly the specialized nail care industry, has experienced a profound structural evolution over the past several decades1. Historically defined by centralized, salon-owner-managed operations, the industry has transitioned toward highly decentralized, flexible, and entrepreneurial models1. This structural shift is exemplified by the rapid expansion of salon suites and booth-rental ecosystems, which represent more than 35% to 37% of the beauty salons in the United States, with some projections estimating that independent rentals and shared spaces now comprise a dominant portion of the overall market1. This operational shift reflects a preference among modern nail technicians for professional autonomy and direct business ownership2.

To analyze the modern nail industry, one must examine the specific characteristics that define how work is performed, how schedules are managed, and how business relations are maintained:

- Technician Mobility and Multi-Salon Access: Modern nail technicians exhibit high geographic and professional mobility2. Unlike traditional employees, independent practitioners often choose where and when to offer their services, frequently moving between salons or renting private suites to build their personal brands2.

- Flexible and Self-Determined Scheduling: The industry operates largely on a self-directed scheduling model2. Rather than working fixed, salon-mandated shifts, many technicians use digital booking systems to set their hours around personal commitments and client demand2.

- Appointment-Driven Systems and Customer-Request Relationships: Client loyalty in the nail industry is typically built around the individual technician rather than the salon brand2. Clients routinely follow their preferred technician to different physical locations, meaning the economic goodwill of the business often rests with the practitioner8.

- Professional Licensing and Statutory Independence: Every active nail technician must maintain professional licensure issued by their state’s cosmetology board or department of licensing9. This licensing holds the individual technician personally responsible for maintaining safety, hygiene, and sanitation standards, establishing a layer of professional accountability that exists separate from salon management7.

- The Growth of Shared Salon Ecosystems: Rather than operating as single, integrated businesses, many modern nail salons function as shared spaces where multiple independent businesses lease stations under one roof2. Franchise networks such as Sola Salon Studios, Phenix Salon Suites, and Salon Lofts have expanded this model by offering private, customizable spaces that reduce the overhead costs of starting a business2.

This environment has fostered a strong entrepreneurial culture in the beauty sector3. Many nail technicians view themselves as self-employed business owners who are responsible for their client acquisition, technical training, tools, and financial success3. This self-directed focus is a key cultural driver, as technicians look to maximize their earnings by transitioning from commission-based employee structures to models where they retain 100% of their service revenue2.

Separating Payment Mechanisms from Worker Classification

A common source of confusion in salon management is the assumption that the payment method used to disburse funds determines the underlying worker classification8. Salon operators and technicians often incorrectly believe that paying a worker in cash, by check, or through a direct deposit system automatically establishes a 1099 independent contractor relationship8.

In regulatory analysis, the mechanism used to transfer funds is separate from the legal classification of the worker8. The legal status of a nail technician—as either a W-2 employee or a 1099 independent contractor—is determined by the operational reality of behavioral control, financial control, and the nature of the relationship, not by the physical or digital payment instrument8.

| Payment Method | Technical Mechanism | Common Industry Perceptions | Regulatory and Compliance Reality |

| Cash[cite: 15, 16] | Direct physical currency exchange between the client and technician or salon15. | Frequently associated with independent contractor status or unreported income15. | Neutral. Cash is simply a payment method8. Both employees and contractors must record and report all cash receipts, including tips, to comply with tax laws18. |

| Check[cite: 8, 10] | Physical paper instrument drawn on a business or individual account8. | Believed to indicate contract-based compensation when issued without tax withholdings8. | Neutral. Checks can represent net wages for employees (reported on Form W-2) or service payments for independent businesses (reported on Form 1099-NEC)14. |

| Direct Deposit & ACH[cite: 22, 23] | Electronic fund transfers routed through the Automated Clearing House network22. | Widely perceived as a mechanism exclusive to corporate or W-2 payroll systems13. | Neutral. Electronic banking is used across all business models, including automated rent collection from contractors or payment distributions to vendors22. |

| Commission Split / Payroll[cite: 13, 20] | Allocation of gross service revenue on a percentage basis (e.g., 60/40)8. | Often viewed as an independent relationship where the technician “keeps their share”8. | Strong W-2 Indicator. The IRS and state tax agencies typically view commission splits with no fixed rent floor as wage compensation, indicating an employee relationship8. |

To maintain compliance, classification discussions should focus on operational behavior rather than payment methods13. If a salon owner sets a technician’s schedule, determines their service prices, and provides their tools, the IRS and state labor agencies will classify the worker as an employee8. This remains true even if the worker is paid via 1099-NEC or in cash8. Conversely, an independent booth renter does not become an employee simply because they use a salon’s shared point-of-sale (POS) system, provided they maintain complete control over their business ledger and client pricing6.

Control as the Primary Operational Observation

The concept of “control” is the primary analytical standard used by federal and state regulators to evaluate worker classification5. This standard is divided into behavioral control, financial control, and the broader economic realities of the working relationship8.

To understand how control operates within a salon, regulators analyze several key questions:

- Schedule Determination: Who decides when the technician works and how many hours they must provide8?

- Time-Off Approvals: Does the technician require management approval to take time off, or do they manage their own availability7?

- Multi-Salon Participation: Is the technician contractually or operationally barred from working at other beauty salons, or do they maintain complete professional mobility8?

- Customer Continuity: Who owns the client list and booking data, and can the technician take their client files if they choose to leave the facility7?

The “right to control” how services are performed carries the greatest weight in these evaluations21. If a salon owner retains the authority to direct how a technician performs a service—rather than simply reviewing the final result—the relationship is classified as employment8.

| Operational Area | Higher Technician Control (Independent Contractor / Renter Indicators) | Lower Technician Control (W-2 Employee / Commission Indicators) |

| Scheduling & Time Off | • Technician sets all working hours8. • No attendance or shift requirements7. • Blocks out time off without approval7. | • Salon dictates work schedules8. • Mandatory attendance or shift coverage8. • Time off requires manager approval8. |

| Pricing & Services | • Technician sets their own service prices8. • Determines which nail services to offer7. • Selects and purchases all product lines1. | • Salon establishes a fixed price list8. • Menu limited to salon-approved services10. • Salon provides and mandates specific products8. |

| Client Management | • Direct access and ownership of client data6. • Freedom to transfer client list to new locations8. • Manages booking independently7. | • Salon owns all client databases and files8. • Enforces non-compete or client-solicitation rules8. • Front desk controls booking and assignments7. |

| Financial Risk & Investment | • Direct payment collection from customers10. • Pays a flat rent regardless of revenue6. • Significant investment in tools and products8. | • Salon collects all customer payments20. • Paid an hourly, salary, or commission wage8. • No capital investment in workspace tools8. |

This behavioral evaluation is supported by federal and state standards, such as California’s 22 CCR Section 4304-12, which defines specific indicators for licensed cosmetologists and barbers27. These rules state that a professional’s ability to set their own hours, establish prices, collect payments directly, and personally resolve client complaints points toward independent status27.

However, state laws vary significantly. Under the strict “ABC” test applied in states like New Jersey, a worker is considered an employee unless the salon can prove that the technician is free from control (Prong A), performs work outside the usual course of business or outside the salon’s physical location (Prong B), and is engaged in an independently established trade (Prong C)24. Because nail services are the core business of a nail salon, booth renters in these jurisdictions are often classified as employees under state labor law, even if they qualify as independent contractors under federal common law24.

Why Industry Participants Associate Autonomy with 1099 Principles

In the beauty and nail salon community, technicians and owners frequently associate operational autonomy with 1099 independent contractor or booth-rental principles10. This association is driven by a shared interest in flexibility and business ownership1.

- Schedule Autonomy as a Career Driver: Many nail technicians enter the beauty industry specifically to manage their own schedules2. The ability to adjust working hours around family commitments, continuing education, or personal needs is viewed as a key benefit of independent work1.

- Professional Mobility and Client Ownership: Technicians often build deep, personal connections with their clients2. Within the industry’s culture, technicians widely believe that if a client base follows a professional to a new location, those clients represent the technician’s personal business asset, not the property of the host salon8.

- Independent Decision-Making: Choosing which product brands, nail art techniques, and sanitizing systems to use is considered an essential professional freedom1. This level of choice is seen as a key aspect of operating an independent business, rather than acting as an employee subject to a salon owner’s directives8.

- Direct Financial Responsibility: The willingness to pay a fixed weekly or monthly rent, purchase professional liability insurance, and cover all business expenses is viewed by technicians as a commitent to running a separate micro-enterprise6.

This focus on business ownership is a major driver of the salon suite trend1. By transitioning from a traditional salon to a private suite, a technician can act as an independent brand, manage their own prices, and retain all revenue, while avoiding the high overhead costs of opening a traditional brick-and-mortar salon2. While state laws ultimately determine legal status, these entrepreneurial characteristics explain why many industry participants associate professional freedom with independent 1099 principles8.

Aligning Documentation with Operational Reality

A common compliance risk for salons is relying on written contracts that do not match how the business actually operates8. Regulatory bodies, such as the IRS and state labor departments, routinely look past written agreements to evaluate the day-to-day behavior of the parties8.

To build a reliable compliance system, documentation must reflect—rather than dictate—actual business behavior7. If a written agreement describes an independent contractor relationship, but the salon owner manages the technician’s schedule and controls customer pricing, the agreement will be set aside during an audit, resulting in reclassification and penalties8.

[ THE DOCUMENTATION PYRAMID ]

▲

╱ ╲

╱ ╲

╱ ╲

╱ RELATION ╲

╱ AGREEMENTS ╲

├──────────────┤

╱ OPERATIONAL ╲

╱ RECORDS ╲

├────────────────────┤

╱ BUSINESS ╲

╱ RECORDS ╲

├──────────────────────────┤

╱ PROFESSIONAL ╲

╱ DOCUMENTS ╲

└────────────────────────────────┘

Professional Documentation

- State Board Licenses: Active professional cosmetology, manicurist, or nail technician licenses issued by the state regulatory authority9.

- Local Business Licenses: Standalone business registrations or tax certificates from the local municipality, establishing the technician’s business entity6.

- Professional Liability Insurance: Personal liability policies held by the technician to cover their services and clients, separate from the salon’s general liability coverage7.

- Certifications & Continuing Education: Records of advanced training, specialty nail art courses, or sanitation certifications completed by the practitioner7.

Business Documentation

- Tax Registrations: Federal Employer Identification Numbers (EIN) or state business tax accounts6.

- Expense & Revenue Ledgers: Independent accounting records, including receipts for product purchases, advertising, and insurance11.

- Tax Forms: IRS Form W-9 to collect tax information, Form 1099-NEC to report independent contractor earnings, and Form 1099-K for digital payments10.

Operational Documentation

- Independent Booking Records: Appointment calendars managed directly by the technician through personal software or client logs7.

- Service & Client Files: Private client records, color formulations, waiver forms, and transaction details owned by the practitioner6.

- Product Purchase Invoices: Invoices showing that the technician purchases their own nail polishes, acrylic products, files, and sanitizing solutions8.

Relationship Documentation

- Station Lease & Booth Agreements: Detailed written contracts specifying the leased space, lease terms, and flat rent amounts7.

- Shared-Services Agreements: Agreements outlining access to shared amenities, such as laundry, Wi-Fi, and waiting areas7.

- Professional Responsibility Acknowledgements: Documents confirming that the technician is responsible for their own tax filings, licensing renewals, and business insurance6.

Structured Communication Framework

To prevent disputes and reduce the risk of worker misclassification, salons and technicians should establish a clear communication framework7. Misunderstandings often arise when the operational boundaries between the host salon and the technician become blurred, or when expectations are left unstated12.

┌───────────────────────────────────────────┐

│ THE DUAL-ENTITY RESOURCE MATRIX │

└─────────────────────┬─────────────────────┘

│

┌──────────────────────────┴──────────────────────────┐

▼ ▼

┌──────────────────────────────────────┐ ┌──────────────────────────────────────┐

│ THE HOST SALON PROVIDES │ │ THE TECHNICIAN PROVIDES │

├──────────────────────────────────────┤ ├──────────────────────────────────────┤

│ • Safe, clean facility & utilities │ │ • Active professional state license │

│ • Maintenance of common shared areas │ │ • Standalone business license & EIN │

│ • Standardized booth rental lease │ │ • Personal tools, products, supplies │

│ • Access to building & shared spaces │ │ • Independent scheduling & booking │

│ • Building security & general cover │ │ • Direct customer billing system │

└──────────────────────────────────────┘ └──────────────────────────────────────┘

A transparent communication model requires both parties to define their respective roles and operational boundaries:

What the Salon Provides

The salon owner acts as a commercial landlord, providing a safe, clean, and fully functional workspace that meets local building and cosmetology board codes11. This includes supplying continuous water, electricity, climate control, and access to common areas such as waiting rooms, restrooms, and break areas7.

What the Technician Provides

The technician acts as an independent business owner, providing all professional tools, implements, nail polishes, acrylic systems, gel lamps, and disposables needed for their services6. They also provide their own business entity registration, active professional licensing, and personal liability insurance6.

Salon Responsibilities

The salon is responsible for maintaining the physical building, managing common area cleanliness, and keeping the commercial property insured11. The salon owner must respect the technician’s independence and avoid managing their schedules, dress codes, pricing, or service methods7.

Technician Responsibilities

The technician is responsible for keeping their rented station clean, sanitizing their tools according to state board rules, and managing their business financials7. This includes filing quarterly estimated taxes, paying rent on time, and directly resolving any customer service issues or complaints11.

Decisions Controlled by the Technician

The technician retains complete control over their business operations21. This includes setting their service prices, determining their working hours, choosing their product brands, selecting which clients to accept, and managing their scheduling platform8.

Protecting the Salon Environment

To protect the shared salon environment and customer safety, both parties must adhere to clear professional standards7. These standards include complying with OSHA ventilation and safety guidelines, maintaining proper waste disposal, following state board sanitation rules, and maintaining professional conduct in shared areas7.

Quarterly Self-Audit Protocol

To prevent gradual shifts in control and ensure that daily behavior matches written contracts, salons and technicians should conduct a formal self-audit each quarter7. Over time, informal adjustments can blur the lines of an independent relationship—such as a salon owner asking an independent renter to help cover the front desk during busy hours, or a contractor relying on salon-provided backbar products8.

This checklist is designed to align with the auditing practices of state and federal regulatory bodies15.

| Audit Category | Operational Review Questions | Goal and Verification | Status |

| Scheduling Control[cite: 8, 27] | • Does the technician set their own hours and block out time without management approval? • Is the technician free from mandatory shifts or floor-coverage hours? | Verifies behavioral independence and scheduling control8. | [ ] |

| Financial Independence[cite: 8, 27] | • Does the technician set their own service prices and menu? • Are customer payments collected directly by the technician? | Verifies financial independence and direct income management8. | [ ] |

| Supplies & Investment[cite: 8, 25] | • Does the technician purchase their own products, nail colors, and tools? • Is the rental fee structured as a flat rate rather than a commission split? | Confirms the technician’s capital investment and business risk8. | [ ] |

| Operational Conduct[cite: 8, 27] | • Is the technician free from mandatory staff meetings and training sessions? • Can the technician work at other locations or salons without restriction? | Verifies there are no employer-like performance expectations8. | [ ] |

| Documentation Alignment[cite: 7, 11, 22] | • Does the technician have an active state cosmetology license and business license? • Is the signed station lease agreement up to date? | Ensures legal and relationship documentation is current6. | [ ] |

Conducting this self-audit on a regular basis helps salons and technicians identify operational changes, update their written agreements, and maintain transparent, consistent, and compliant business relationships7.

Compliance Through Operational Understanding

Real and lasting compliance is not achieved by using legal terminology to mask control8. Instead, it is built on a clear alignment of transparency, open communication, consistent daily behavior, and accurate documentation7.

[ THE COLLABORATIVE COMPLIANCE CYCLE ]

│

┌────────────────────────────┼────────────────────────────┐

▼ ▼ ▼

┌──────────────────────┐ ┌──────────────────────┐ ┌──────────────────────┐

│ TRANSPARENCY │ │ CONSISTENCY │ │ UNDERSTANDING │

├──────────────────────┤ ├──────────────────────┤ ├──────────────────────┤

│Both parties openly │ │Daily operations are │ │Both parties know the │

│discuss and agree to │ │monitored to ensure │ │legal distinctions, │

│the financial and │ │they match written │ │responsibilities, │

│operational bounds. │ │contract terms. │ │and audit standards. │

└──────────────────────┘ └──────────────────────┘ └──────────────────────┘

Misunderstandings and compliance risks typically occur when these core elements are missing:

- Undocumented Operational Realities: In cash-intensive businesses like nail salons, failing to keep accurate ledgers, receipts, and appointment records can trigger audit scrutiny15. The IRS Audit Technique Guide (ATG) for beauty salons instructs auditors to reconstruct income using appointment books, price lists, and industry averages if clear financial records are missing15.

- Uncommunicated Expectations: When salon owners and technicians do not openly discuss their respective roles, friction often arises over product usage, building access, and client booking ownership7.

- Contracts That Do Not Match Behavior: If a salon uses an independent contractor agreement but treats the technician as an employee, tax and labor authorities will reclassify the relationship during an audit8. This can result in significant financial penalties, including unpaid payroll taxes, interest, and fines21.

To support compliance, federal programs like the IRS Tip Reporting Alternative Commitment (TRAC) emphasize voluntary education and structured documentation18. Under a TRAC agreement, salon owners commit to educating workers on proper tip reporting and maintaining detailed records, which helps reduce audit risk and improve compliance through clear communication rather than enforcement18.

Final Conclusion

Establishing a compliant and successful salon environment requires a clear, sequential approach to structuring professional relationships:

Compliance cannot be achieved by using written contracts to obscure the reality of how a business operates8. Instead, it requires that the day-to-day behavior of both parties matches their chosen business model, supported by clear communication and accurate documentation7.

The objective of this analysis is not to advocate for a single worker classification, but to provide salon owners, technicians, educators, and compliance professionals with a clear framework to evaluate, document, and manage their business relationships with transparency, professional responsibility, and regulatory alignment11.

Works cited

- Suite Rental Trend Growing Quickly in California – Salon Success Academy, https://www.salonsuccessacademy.com/blog/suite-rental-trend-growing-quickly-in-california/

- The Rising Demand for Salon Suites: Market Trends and Statistics, https://salonrenter.com/rising-demand-salon-suites-market-trends-statistics/

- Why individual salon suites are revolutionizing the beauty industry, https://optimasalons.com/why-individual-salon-suites-are-revolutionizing-the-beauty-industry/

- The Growth of Independent Salon Owners: Industry Insights, https://salonrenter.com/growth-of-independent-salon-owners/

- W-2 Employees vs 1099 Independent Contractors, https://eliteaae.com/blogs/exclusive-blogs/w-2-vs-1099-in-the-aesthetic-industry

- Employee vs Booth Renter vs Independent Contractor: Key Differences in the Salon Industry, https://biz.booksy.com/en-us/blog/employee-vs-booth-renter-vs-independent-contractor-key-differences-in-the-salon-industry

- Booth Rental Agreement Template (Free Download + AI Generator) – AI Lawyer, https://ailawyer.pro/blog/booth-rental-agreement-template-(free-download-ai-generator)

- Salon 1099 vs W-2 in Texas: IRS Rules for 2026 – The Local Gem, https://www.thelocalgem.com/blog/salon-1099-vs-w-2-in-texas-irs-rules-for-2026

- Specific licensing requirements | Washington Department of Revenue, https://dor.wa.gov/education/industry-guides/beauty-and-wellness-services/specific-licensing-requirements

- Know Your Workers’ Rights – California Board of Barbering and Cosmetology, https://www.barbercosmo.ca.gov/about_us/meetings/materials/20170626_mm.pdf

- Salon Owner & Booth Renter Responsibilities: Rules, Roles, and Rights – Booksy Biz, https://biz.booksy.com/en-us/blog/salon-owner-booth-renter-responsibilities-rules-roles-and-rights

- Contract Labor, Booth Renter, or Employee — What Are They Really? – NAILS Magazine, https://www.nailsmag.com/390523/contract-labor-booth-renter-or-employee-what-are-they-really

- Commission vs Booth Rental: The Complete Comparison for Salon Owners – Vagaro, https://www.vagaro.com/learn/salon-commission-vs-booth-rental-guide

- Independent contractor (self-employed) or employee? | Internal Revenue Service, https://www.irs.gov/businesses/small-businesses-self-employed/independent-contractor-self-employed-or-employee

- Tax Audits of Cash Intensive Businesses | Los Angeles Tax Services Lawyers, https://www.lataxattorney.com/practice-areas/tax-audits/tax-audits-of-cash-intensive-businesses/

- IRS Cash Audit Techniques Guide – christy pinheiro, http://www.christypinheiro.com/uploads/1/7/9/2/179206/cash_audit_techniques_guide.pdf

- 24703 HON. NICK LAMPSON HON. NANCY L. JOHNSON HON. JULIAN C. DIXON – GovInfo, https://www.govinfo.gov/content/pkg/CRECB-2000-pt17/pdf/CRECB-2000-pt17-Pg24703-3.pdf

- Items of General Interest Proposed Revised Tip Reporting Alternative Commitment (TRAC) Agreement for Use in the Cosmetology – IRS, https://www.irs.gov/pub/irs-drop/a-00-21.pdf

- Is Your Salon on the IRS Radar? Red Flags That Trigger Audits! -, https://fas-accountingsolutions.com/is-your-salon-on-the-irs-radar-red-flags-that-trigger-audits/

- Form 14430-A SS-8 Determination—Determination for Public Inspection – IRS, https://www.irs.gov/pub/ss8/05PCP130615.pdf

- Employee or Independent Contractor? – Centre for Beauty, https://cjscentreforbeauty.com/employee-or-independent-contractor/

- Booth Rental Salon Agreements: Examples and Best Practices – Boulevard, https://www.joinblvd.com/blog/booth-rental-salon-agreement

- Salon Booth Rental Agreement Forms Examples (With PDF) – Vagaro, https://www.vagaro.com/learn/booth-rental-agreement-forms-explained

- Accounting & Tax for Salons and Spas – Monaco CPA, https://www.monacocpa.cpa/industries/salons-spas

- Booth Rental Contract: What is it? Key Terms, Considerations – ContractsCounsel, https://www.contractscounsel.com/t/us/booth-rental-contract

- DOL Shelves Independent Contractor Rule | Epstein Becker Green, https://www.wagehourblog.com/dol-shelves-independent-contractor-rule

- Cal. Code Regs. Tit. 22, §§ 4304-12 – Specific Application of Rules for Determination of Employment Status to Circumstances in the Barbering and Cosmetology Industry | State Regulations, https://www.law.cornell.edu/regulations/california/22-CCR-4304-12

- Tax Filing Tips for Hair Salons, Barbers, and Hairdressers – TurboTax – Intuit, https://turbotax.intuit.com/tax-tips/self-employment-taxes/work-as-a-hair-stylist-tax-tips-for-hairdressers/L2do5YTxP

- 5+ FREE Subcontractor Safety Plan Samples to Download, https://www.sample.net/business/plans/subcontractor-safety-plan/

- IRS Audit Guides | Tax Collection Relief, https://www.taxcollectionrelief.com/irs-audit-guides

IMPORTANT DISCLAIMER, RESEARCH ATTRIBUTION, AND LIMITATION OF LIABILITY

Educational Publication Notice

This publication is provided solely for educational, informational, workforce-development, public-discussion, and research purposes.

The content contained herein does not constitute legal advice, tax advice, accounting advice, labor-law advice, regulatory advice, human-resources advice, compliance advice, or professional consulting services of any kind.

Readers should consult qualified attorneys, certified public accountants (CPAs), tax professionals, labor-law specialists, insurance professionals, and applicable government agencies before making any business, employment, tax, payroll, licensing, insurance, worker-classification, or compliance decisions.

Research Attribution

This study, analysis, framework, observations, commentary, interpretations, and conclusions were independently researched, developed, compiled, and prepared by:

Di Tran University

The College of Humanization

Di Tran University Research Team

All research methodologies, observations, analyses, interpretations, educational frameworks, and conclusions expressed in this publication belong solely to the Di Tran University Research Team.

Louisville Beauty Academy did not prepare, author, certify, validate, endorse, guarantee, or provide legal review of the research findings, interpretations, observations, or conclusions contained herein.

Louisville Beauty Academy serves solely as an educational publisher, educational platform, workforce-development institution, and distribution channel for public discussion and educational purposes.

Observational Study Disclaimer

This publication is an observational and educational study.

The study is intended to examine commonly observed operational practices, business models, workforce behaviors, communication systems, documentation practices, and professional relationships within portions of the beauty industry.

Descriptions of industry practices, behaviors, customs, trends, or commonly observed business arrangements are presented for educational discussion only and should not be interpreted as legal determinations, regulatory findings, government positions, compliance certifications, or legal conclusions.

Any references to worker classification principles, operational autonomy, independent-professional relationships, salon ecosystems, booth-rental arrangements, contractor relationships, employee relationships, or compliance considerations are presented solely as educational observations and analytical discussion.

No Classification Determination

Nothing in this publication should be interpreted as determining, certifying, recommending, approving, or guaranteeing any worker classification.

No statement contained herein should be interpreted to mean that any specific worker, salon, business, owner, manager, technician, contractor, renter, or professional is properly classified under any federal, state, or local law.

Worker classification determinations depend upon applicable laws, regulations, facts, circumstances, jurisdiction-specific requirements, regulatory interpretations, and governmental review.

Only the appropriate governmental authorities, courts, administrative agencies, and licensed legal professionals may provide authoritative determinations regarding worker classification.

No Guarantee of Compliance

This publication makes no representation, warranty, guarantee, or promise that following any observation, framework, recommendation, checklist, documentation practice, communication system, or business procedure discussed herein will result in legal compliance, tax compliance, regulatory compliance, worker-classification compliance, audit protection, or favorable governmental determinations.

Compliance outcomes depend upon numerous factors beyond the scope of this publication.

Hold Harmless Provision

By reading, referencing, sharing, citing, or relying upon this publication, readers acknowledge that they assume full responsibility for any decisions, actions, interpretations, business practices, legal conclusions, tax positions, employment practices, or compliance strategies they may adopt.

Neither Louisville Beauty Academy, Di Tran University, the College of Humanization, Di Tran University Research Team, nor any affiliated contributors shall be liable for any direct, indirect, incidental, consequential, regulatory, tax, employment, labor, licensing, insurance, or legal outcomes arising from the use of this publication.

Educational Mission

The purpose of this publication is simple:

To encourage transparency.

To encourage documentation.

To encourage communication.

To encourage professional responsibility.

To encourage informed discussion.

To better understand the operational realities of the beauty industry.

Published for educational purposes by Louisville Beauty Academy.

Research conducted independently by Di Tran University Research Team, The College of Humanization.

© Di Tran University Research Team. All research rights reserved.