Disclaimer: This publication is provided solely for educational, research, and public-interest discussion by Louisville Beauty Academy (LBA) and Di Tran University (DTU). It is intended to promote understanding of beauty education, public safety, sanitation, occupational licensing, administrative law, due process, regulatory transparency, and professional responsibility. The content reflects research, publicly available laws, regulations, court decisions, government publications, academic literature, and policy analyses available at the time of publication. It is not legal advice, does not accuse or imply misconduct by any individual, agency, board, school, or organization, and should not be interpreted as a statement regarding any specific person or pending matter. Laws and regulations vary by jurisdiction and may change over time; readers should consult the applicable statutes, regulations, licensing authorities, or qualified legal counsel regarding their specific circumstances. LBA and DTU fully support lawful regulation that protects public health, safety, sanitation, consumer welfare, ethical education, and professional excellence, while also encouraging transparency, fairness, evidence-based policymaking, due process, equal access, and continuous improvement for the benefit of students, licensees, educators, regulators, and the public.

The regulation of the American beauty industry — encompassing cosmetology, nail technology, esthetics, shampoo styling, instructor licensing, and beauty schools — represents one of the most complex, heavily layered, and least publicly understood systems of occupational governance in the United States. At its best, this regulatory architecture protects the public from infection, chemical injury, and incompetent practice. At its worst, it has functioned as a barrier to economic participation for immigrants, low-income workers, people of color, and non-English speakers — without producing commensurate gains in public safety.

This study examines the origins, evolution, and contemporary operation of beauty industry regulation with equal weight given to its protective functions and its recorded harms. It draws on constitutional law, administrative law, public policy scholarship, historical research, federal agency findings, state board rules, and court decisions. It concludes with a practical due process framework and positions Louisville Beauty Academy and Di Tran University as institutions of excellence in integrated compliance, sanitation, and rights-aware beauty education.

The core research question — whether beauty regulation serves public safety or also serves as a tool of control over vulnerable populations — cannot be answered with a simple yes or no. Both are true, and the productive response is not cynicism but informed, empowered professionalism.

Part I: Historical Roots of Beauty Industry Regulation

1.1 Origins: The Early Twentieth Century

The formal regulation of cosmetology and barbering in the United States emerged primarily in the 1920s through the 1940s, driven by a confluence of genuine public health concerns, professional ambition, and social dynamics that have shaped the industry ever since. Illinois enacted one of the first comprehensive state licensing laws for beauty culture practitioners in 1925, establishing original requirements covering examinations, fees, renewal, and reciprocity. California separately licensed barbers and cosmetologists beginning in 1927, reflecting both a social and professional divide that would persist for decades. North Dakota passed its first act to regulate hairdressers and cosmetologists in 1927, creating a State Board of Hairdressers and Cosmetologists to oversee the profession. South Carolina established its State Board of Cosmetic Art Examiners in 1934, and Mississippi created its Board of Cosmetology in 1948.[1][2][3][4][^5]

The stated rationale in nearly every state was uniform: protect consumers from unsanitary practices, communicable diseases, and chemical injuries that genuine hands-on beauty work could produce. This rationale had real merit. Early salons used harsh chemical compounds with limited safety knowledge, shared instruments without disinfection between clients, and operated in conditions that could spread ringworm, bacterial infections, and other skin diseases. Public health considerations were not fabricated — they were real.[^6]

1.2 The Role of Sanitation and Public Health

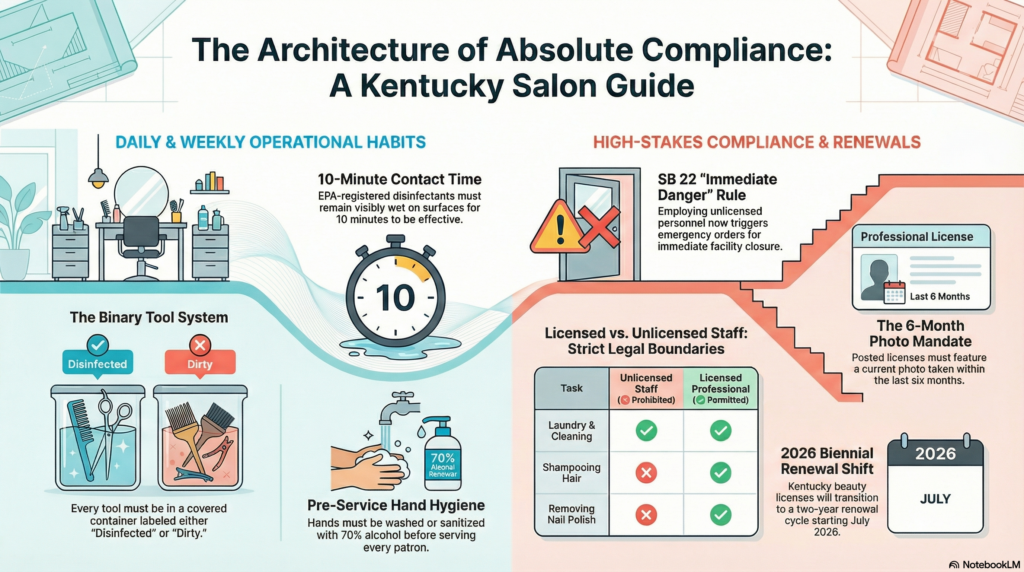

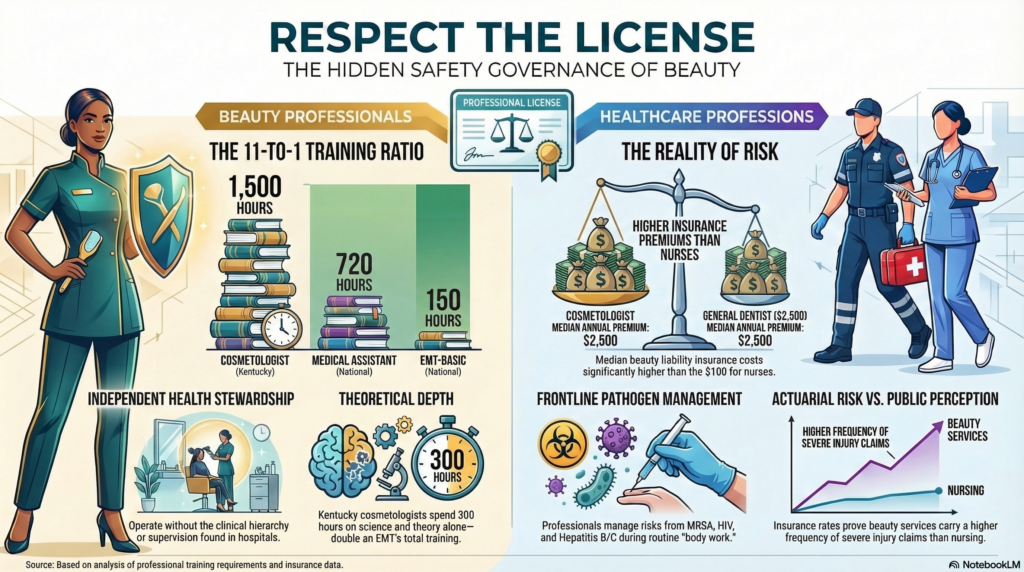

Sanitation remains the bedrock justification for beauty licensing and is the area where regulation most clearly serves its stated mission. Professional beauty services create documented opportunities for disease transmission: shared implements can spread bacterial infections, fungal conditions such as tinea capitis or onychomycosis, and blood-borne pathogens if skin is broken. Pedicure basins, nail tools, and facial instruments are particularly high-risk vectors if not properly disinfected. The requirement that professionals demonstrate competence in disinfection, sanitation protocols, and safe chemical handling before serving the public is therefore rationally connected to a legitimate government interest in preventing harm.[7][6]

Regulatory bodies including state boards of cosmetology mandate specific disinfection protocols — EPA-registered disinfectants, proper contact times, documented pedicure basin logs, and safe chemical storage — precisely because these protections have a direct connection to client health and safety. The Federal Food, Drug, and Cosmetic Act of 1938 established early federal oversight of cosmetic products, and the Modernization of Cosmetics Regulation Act of 2022 (MoCRA) — the most significant expansion of FDA authority over cosmetics since 1938 — updated requirements for adverse event reporting, safety substantiation, mandatory recall authority, and Good Manufacturing Practices. These are serious public protections deserving respect.[8][9]

1.3 The Expansion of Licensing: From Safety to Social Control

Yet the historical record reveals a more complicated picture. Licensing laws were not solely driven by public health. Academic research on the licensing of barbers and beauticians documents how these laws were shaped by competitive interests, racial stratification, and the desire of established practitioners to control market access. One of the clearest examples: early barber licensing laws in numerous states were explicitly deployed to suppress Black competition. Georgia’s Jim Crow barber codes prohibited colored barbers from serving white women and girls. Barbering had been one of the first skilled trades African Americans mastered in America, but the introduction of formal licensing in the late nineteenth and early twentieth centuries coincided with Jim Crow-era exclusions that systematically restricted Black entry into licensed trades. Licensing laws — generally framed in race-neutral language — had racially discriminatory effects both North and South, used as tools to prevent Black workers from competing with established white practitioners.[10][11][12][13]

This history is not merely retrospective. It established a template in which licensing requirements could be structured to disadvantage workers without explicitly targeting them — a pattern that would recur across generations with immigrant workers, low-income applicants, and non-English speakers.

Part II: The Regulatory Architecture — Who Governs Beauty?

2.1 State Boards as the Primary Governors

In the United States, the beauty industry is regulated almost entirely at the state level. All fifty states plus the District of Columbia require a license to practice cosmetology. Every state maintains a cosmetology board, barbering board, or combined professional licensing body that exercises authority over: individual practitioner licenses (cosmetologist, nail technician, esthetician, shampoo technician, instructor); salon and school establishment licenses; curriculum standards for schools; examinations; inspection and enforcement; complaint processing; disciplinary actions; and license renewals. Some states regulate manicuring, esthetics, and shampoo styling as distinct licenses with separate hour and examination requirements.[14][15][^16]

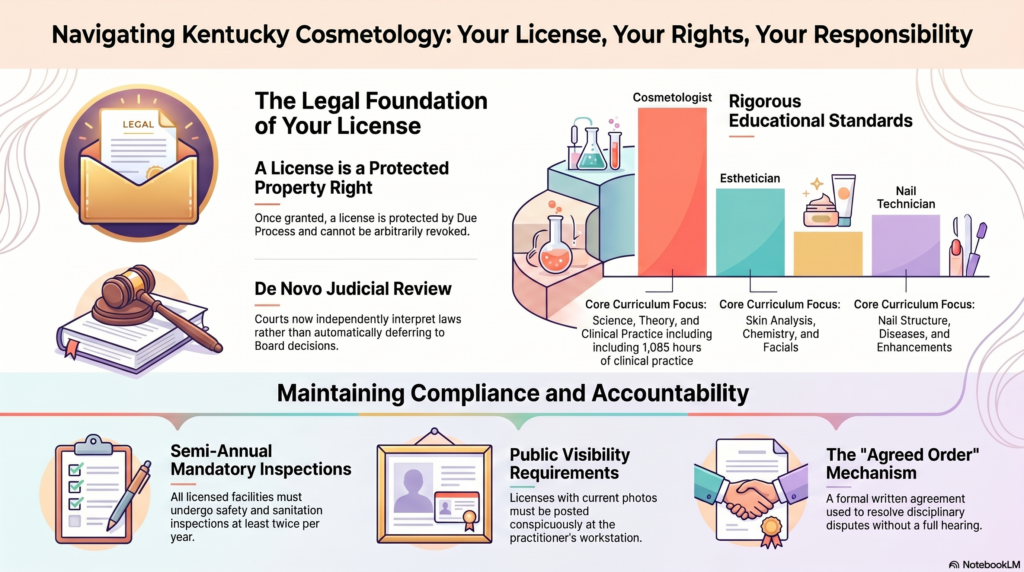

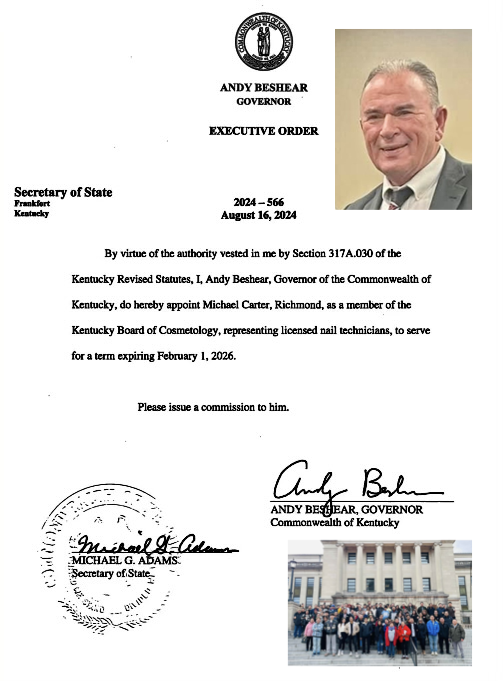

The Kentucky Board of Cosmetology, to cite the home jurisdiction of Louisville Beauty Academy, administers KRS Chapter 317A and 201 KAR Chapter 12, which govern cosmetology, nail technology, threading, eyelash artistry, makeup artistry, and esthetics. It requires a minimum of two inspections per year of each licensed establishment, empowers board members and inspectors to enter licensed premises during reasonable working hours, and requires establishments to produce records for inspection and copying. These powers are broad and, for the uninformed licensee, can feel overwhelming.[^17]

2.2 Federal Oversight: A Limited but Growing Role

At the federal level, the Food and Drug Administration (FDA) regulates cosmetic products — the chemical substances used in professional services — but historically exercised limited authority over the beauty profession itself. MoCRA (2022) expanded FDA’s product oversight significantly, requiring facility registration, product listing, adverse event reporting, and safety substantiation records. The Department of Education exercises oversight through Title IV financial aid administration, which conditions federal student loan and Pell Grant eligibility on school accreditation. NACCAS (National Accrediting Commission of Career Arts & Sciences) serves as the primary institutional accreditor for cosmetology schools seeking Title IV eligibility. The Federal Trade Commission monitors occupational licensing boards for anti-competitive practices, most famously after North Carolina State Board of Dental Examiners v. FTC, 574 U.S. 494 (2015), which held that state licensing boards dominated by active market participants are subject to federal antitrust law unless actively supervised by the state.[18][19][20][8]

2.3 The Regulatory Layering Problem

A beauty school owner in Kentucky, for example, faces regulatory obligations from the following authorities simultaneously:

- Kentucky Board of Cosmetology (KRS 317A / 201 KAR 12): state licensure, school approval, curriculum hours, instructor credentials, inspection compliance, sanitation standards, student record-keeping, hour-tracking documentation

- NACCAS: accreditation standards covering educational objectives, instructional staff, admissions policies, student support services, curriculum, financial practices, facilities, and student evaluations[21][22]

- U.S. Department of Education: Title IV financial aid administration, satisfactory academic progress standards, return-to-title-IV (R2T4) calculations, cohort default rates, gainful employment[^23]

- Kentucky Administrative Procedure Act (KRS 13B): administrative hearing procedures applicable to any disciplinary action

- OSHA and EPA: workplace safety and chemical handling regulations for schools and salons

- State and local business licensing: general business operation requirements

- Local fire, zoning, and building codes: physical plant requirements

The cumulative documentation, compliance, and legal-knowledge burden placed on a single owner-operator — who in many cases is an immigrant, a first-generation entrepreneur, or a person operating with limited financial resources — is extraordinary by any objective measure.

Part III: The Regulatory Burden — A Comparative Analysis

3.1 Hours Required: Beauty vs. Other Professions

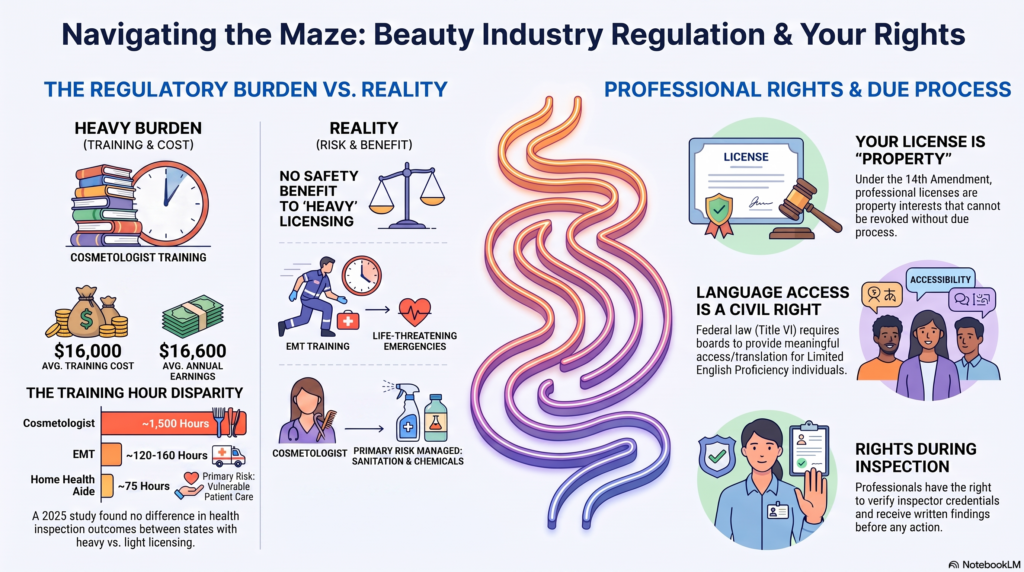

The training hour requirements for beauty professionals are among the most frequently cited evidence that occupational licensing in this sector has exceeded any rational public safety justification. Consider this comparative data:

| Occupation | Average Training Required | Notes |

| Cosmetologist | ~372 training days (~1,500 hours) | Range: 1,000–2,100 hours depending on state [24][25] |

| Emergency Medical Technician (EMT) | ~33 training days (~120-160 hours) | Responds to life-threatening emergencies [25][26] |

| Barber | ~1,000–1,500 hours | Varies by state [^27] |

| Nail Technician | ~300–600 hours | Varies by state |

| Esthetician | ~260–1,500 hours | Varies significantly by state |

| Cosmetology Instructor | ~300–1,000 hours of instructor training (plus underlying license) | [28][29] |

| Home Health Aide | ~75 hours (federal minimum) | Works with vulnerable patients |

| Childcare Worker | Varies; many states 0–12 hours | Cares for children daily |

| Interior Designer | No federal license; some state certifications | Affects structural safety |

| Construction Laborer (non-electrical) | Often no state license | Various safety risks |

As President Trump noted in 2019 remarks to governors, cosmetologists train on average eleven times longer than emergency medical technicians. The Washington Post fact-checked and verified this claim: “on average, cosmetologists do train a little over 10 times as long as EMTs”. A report by the National Conference of State Legislatures confirmed that “cosmetologists require an average of 372 training days, significantly higher than emergency medical technicians, who need an average of 33 training days”.[25][26]

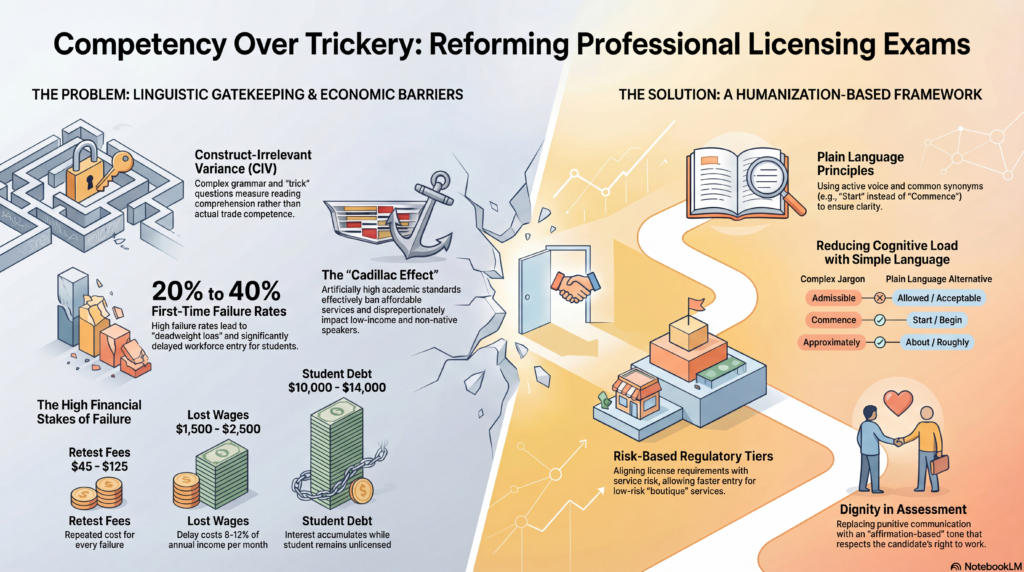

This disparity is not easily explained by reference to public safety. While beauty services do carry real sanitation risks, they rarely involve life-threatening emergencies of the kind EMTs manage daily. The 2015 Obama White House report — prepared jointly by the Department of the Treasury, the Council of Economic Advisers, and the Department of Labor — concluded that licensing can “impose substantial costs on job seekers, consumers, and the economy more generally,” that the percentage of workers requiring a license has increased five-fold since the 1950s, and that over-licensing “disproportionately affects certain populations, including immigrants and anyone with a criminal history”.[30][31]

3.2 The Institute for Justice’s Clean Cut Study (2025)

The Institute for Justice’s April 2025 study, Clean Cut, analyzed whether nail salons and barbershops in states with different licensing burdens had better or worse health inspection outcomes. The finding was unambiguous: “There was no difference in inspection outcomes across the states.” Researchers found that barbershops and nail salons were clean and safe regardless of whether their workers faced burdensome licensing, lighter licensing, or no licensing at all. This study directly challenges the claim that heavier training hour requirements produce better public health outcomes in the beauty industry.[^32]

3.3 Financial Barriers and Student Debt

The cost of entering the beauty profession is substantial. On average, completing the required training for a cosmetology license costs more than $16,000, according to Institute for Justice research, and students took out over $7,300 on average in student loan debt to finance this training. Tuition alone typically ranges from $5,000 to $20,000+ depending on school and location. The total cost including exam fees and licensing application fees typically reaches $6,000–$22,000+.[24][16]

Yet the Brookings Institution reported that cosmetology graduates have average earnings of approximately $16,600, with $9,900 in debt. At the median cosmetology school, 32 percent of students are at least three months behind on their loan payments. A 2026 Department of Education analysis projected that more than 92% of all cosmetology, barber, and related personal grooming programs would fail a proposed earnings accountability test comparing graduate earnings to those of high school graduates. These numbers reflect a systemic tension: students are required by law to attend expensive, time-consuming licensed programs in order to work in a field that is already economically modest.[33][34][^35]

Part IV: The Dark Side — Control, Fear, and Vulnerability

4.1 Immigrants and the Beauty Industry

The American nail salon industry is predominantly owned and staffed by foreign-born individuals — immigrants or refugees running small, family-operated businesses. Vietnamese Americans, following the influence of actress Tippi Hedren who encouraged Vietnamese refugee women to learn nail care in the 1970s, came to dominate the nail salon industry particularly in California and across the country. Research by the UCLA Labor Center and others documents the compound vulnerabilities these workers face: low wages, toxic chemical exposure, limited English proficiency, regulatory complexity they cannot easily navigate, and structural inequities that simultaneously require compliance with English-language law while failing to provide those laws in accessible translated form.[36][37][^38]

A 2023 Federal Reserve Bank of Minneapolis study found that licensure reduces foreign-born employment in a licensed occupation by nearly 20 percent relative to native-born employment — a direct wage and employment penalty for immigrants navigating a licensing system designed around English-language documentation and examination. The study found corresponding wage premiums, consistent with the interpretation that licensing constitutes a disproportionate barrier to the labor supply of immigrants. Research by the CDC confirms that nail salon workers — predominantly immigrant women — face multiple barriers to accessing occupational health training and services, including language barriers, literacy barriers, and lack of culturally appropriate materials.[39][40]

4.2 Language Access Rights: What the Law Requires

Under Title VI of the Civil Rights Act of 1964 and Executive Order 13166 (2000), any entity receiving federal financial assistance — including state licensing boards that participate in federal programs — must take reasonable steps to ensure meaningful access to services for persons with Limited English Proficiency (LEP). “Language access” means providing LEP individuals the same access to government services as English-speaking individuals. Vital documents — those necessary for meaningful access to programs — must be translated into the languages of regularly encountered LEP groups.[^41]

In practice, many state cosmetology boards offer limited or no translation services for inspections, hearings, complaint responses, or licensing examinations. The California Board of Barbering and Cosmetology does offer consumer complaint forms in Korean, Spanish, and Vietnamese — a practice that should be recognized as a best-practice baseline that all boards should meet. The U.S. Commission on Civil Rights approved a report on language access for LEP individuals in February 2026, transmitting findings to the President and Congress. Beauty professionals and their advocates should invoke this federal framework when demanding translated notices, translated complaint forms, and interpreter access in regulatory proceedings.[42][43]

4.3 The Power Imbalance in Regulatory Encounters

State cosmetology boards hold extraordinary power over licensees. Under KRS 317A, any board member, administrator, or inspector may enter any licensed establishment during reasonable working hours. Boards may require production of records, books, and papers pertaining to licensed activity. Boards may impose fines, suspend or revoke licenses, impose probation, and issue public reprimands. In states like Kentucky, the passage of SB22 created the specific category of “immediate and present danger to the public” triggered by the knowing employment of unlicensed persons — a phrase that, if triggered, can result in emergency orders closing a business on the spot.[44][45][^17]

For the vast majority of licensees who have limited legal education, limited English fluency, limited financial resources to hire attorneys, and limited knowledge of their rights under administrative law, this power asymmetry is profound. A licensee who does not know that they are entitled to written notice before disciplinary action, that they have a deadline to respond, that they may appeal, and that silence or panic can be misinterpreted as admission — is a licensee who is structurally vulnerable to erroneous or disproportionate regulatory action.

4.4 Regulatory Capture and Incumbent Protection

A well-documented problem in occupational licensing generally — and in beauty regulation specifically — is regulatory capture: the tendency of licensing boards dominated by active market participants to use their regulatory power to suppress competition rather than protect the public. The Supreme Court’s landmark decision in North Carolina State Board of Dental Examiners v. FTC, 574 U.S. 494 (2015) — while involving dentistry — directly and explicitly addressed this risk in the context of professional licensing boards composed of active market participants. The Court held 6-3 that a state licensing board dominated by active practitioners can invoke state-action antitrust immunity only if it is actively supervised by the state — precisely because the risk of boards using regulatory power to protect incumbents from competition is constitutionally significant.[46][47][48][20][^49]

Research by conservative and libertarian policy organizations (Heritage Foundation, Cato Institute, Goldwater Institute, Institute for Justice) and centrist and progressive bodies (Brookings Institution, Hamilton Project, Obama White House) alike confirms that incumbent businesses endorse licensing requirements precisely because those requirements protect them against competition from new entrants. The Federal Trade Commission has long advocated for reform, noting that “unnecessary licensing restrictions erect significant barriers and impose costs that cause real harm to American workers, employers, consumers, and our economy as a whole, with no measurable benefits to consumers or society”.[50][51][^52]

Beauty schools themselves are not immune from this dynamic. When established schools use accreditation standards, minimum hour requirements, and regulatory lobbying to raise barriers against new competitors — rather than to improve educational quality — they participate in the same incumbent-protection cycle they may simultaneously criticize when boards do it to individual practitioners.

Part V: Administrative Law and Due Process in Beauty Regulation

5.1 Constitutional Foundations

Every licensee in the United States — every cosmetologist, nail technician, esthetician, salon owner, instructor, and school — holds a property interest and a liberty interest in their professional license. The Supreme Court established in Board of Regents v. Roth, 408 U.S. 564 (1972) that professional licenses constitute property interests protected by the Due Process Clause of the Fourteenth Amendment, which prohibits any state from depriving a person of life, liberty, or property without due process of law. The Fifth Amendment independently provides that the federal government cannot deprive any person of life, liberty, or property without following certain procedures.[^53]

Due process in licensing disciplinary proceedings does not require a full court trial, but it does require meaningful procedural protections. The governing constitutional standard is the three-part Mathews v. Eldridge balancing test established by the Supreme Court in 424 U.S. 319 (1976). Under this test, the minimum process required is determined by weighing: (1) the private interest affected by the government action; (2) the risk of erroneous deprivation through the procedures used, and the value of additional safeguards; and (3) the government’s interest, including the administrative burden of additional procedures.[54][55][56][57]

For a licensee facing suspension or revocation — the deprivation of their means of livelihood — the private interest is enormous. The risk of erroneous deprivation in complex regulatory proceedings without legal representation is substantial. Courts have therefore consistently recognized that licensees are entitled to: notice of the specific charges against them, a meaningful opportunity to be heard before adverse action takes effect (or at least promptly thereafter), the right to present evidence and witnesses, and the right to receive written reasons for any adverse decision.[58][59]

5.2 The Administrative Procedure Framework

State administrative procedure acts govern how beauty boards may conduct investigations, issue charges, hold hearings, and impose discipline. In Kentucky, KRS Chapter 13B (the Kentucky Administrative Procedure Act) governs all contested case proceedings before state administrative agencies, including the Kentucky Board of Cosmetology. In Tennessee, the Tennessee Administrative Procedure Act (Title 4, Chapter 5, Tennessee Code Annotated) similarly governs all board disciplinary proceedings.[60][61]

These acts uniformly require: written notice of charges before adverse action; an opportunity to respond to allegations in writing; a hearing before an impartial decision-maker; the right to be represented by an attorney; the right to present witnesses and cross-examine adverse witnesses; a written decision based on findings of fact and legal conclusions; and the right to appeal to a court.[62][63]

In California, the Board of Barbering and Cosmetology’s administrative appeal regulations (16 Cal. Code Regs. § 973.6) specifically provide that a licensee who receives an immediate suspension has 30 calendar days to request an informal review hearing, may bring legal counsel, may present written information and oral testimony, may contest the occurrence of the violation, the period for correction, or the amount of the fine.[^64]

In Kentucky, under 201 KAR 12:190, before any disciplinary action is taken against a licensee, the licensee has the right to: written notice; written citation of the law alleged to have been violated; written statement of the factual basis; a written right to respond; and an opportunity for a hearing. Critically, under Kentucky law, “imminent danger” — the trigger for emergency orders — means unlicensed practice, not confusion, misunderstanding, or paperwork errors. For ordinary sanitation violations and minor paperwork issues, the board must first issue a written warning and provide an opportunity to correct before imposing a fine.[45][60]

5.3 Open Records as a Defensive Tool

Every state has open records or freedom of information laws that give citizens the right to inspect government records, including records maintained by state cosmetology boards. The Kentucky Open Records Act (KRS Chapter 61) allows residents of Kentucky to submit requests for records, including inspection reports, investigator notes, complaint files, and meeting minutes. The Tennessee Public Records Act provides that “all state, county and municipal records shall at all times during business hours be open for personal inspection by any citizen of this state”.[65][66][^67]

These laws are powerful defensive tools for licensees and school owners who face regulatory action. A licensee who suspects that an inspection finding is inaccurate or that a fine was not lawfully approved can use an open records request to obtain the original inspector’s notes, the complaint files, the board meeting minutes approving the fine, and any other relevant documentation. If the minutes show the fine was never formally approved, the fine may be unenforceable. This is not a loophole — it is the rule of law applied to administrative power.[^45]

Part VI: The Regulatory Framework State by State — Key Comparisons

6.1 Training Hours: The Range Across States

Training requirements vary dramatically across states, with no consistent evidence that more hours produce better safety outcomes:

| State | Cosmetologist Hours | Nail Tech Hours | Esthetics Hours |

| Oregon | 2,100 | 300+ | 500 |

| Iowa, Kansas | 1,800 | varies | varies |

| Arizona, Colorado, Wisconsin | 1,600 | 600 | 600 |

| California, Texas, Illinois, Georgia | 1,500 (CA reduced to 1,000 via SB 803) | 400 | 600 |

| Florida | 1,200 | 240 | 260 |

| New York, Massachusetts | 1,000 | 250 | 600 |

California’s Senate Bill 803 (effective 2022) reduced cosmetology training requirements from 1,600 to 1,000 hours specifically to make the industry more accessible. This reform, supported by evidence that 1,000-hour programs produce licensed professionals equally capable of passing state board examinations as 1,600-hour programs, represents a national model for evidence-based regulatory reform.[^68]

6.2 Inspection and Enforcement Comparisons

State inspection practices vary in frequency, documentation requirements, and enforcement philosophy. Kentucky mandates a minimum of two inspections per year per licensed establishment. Other states have annual inspection requirements or complaint-driven inspection schedules. The consistency with which inspections are documented, findings are written, correction periods are granted, and appeal rights are explained varies widely from state to state and in practice from inspector to inspector.[^17]

6.3 Complaint and Disciplinary Systems

Most state boards maintain formal complaint processes, though the accessibility of these processes to non-English speakers varies significantly. Arizona’s Board of Barbering and Cosmetology publishes disciplinary action records and clearly lists the legal bases for disciplinary action. California offers complaint forms in Korean, Spanish, and Vietnamese. The National Accrediting Commission of Career Arts & Sciences (NACCAS) requires accredited schools to maintain formal written complaint procedures that students are made aware of, with escalation paths from the school to the state board to NACCAS to the Department of Education.[69][42][^44]

Under NACCAS standards, students at accredited schools are entitled to: a written complaint form; a defined response timeline (typically 10 calendar days for initial response); escalation to state boards; escalation to NACCAS; and escalation to the Department of Education if unresolved. Schools must teach students about state board requirements, state law, and students must be made aware of licensure requirements prior to enrollment.[22][69]

Part VII: Education Reform — Teaching Law, Not Just Technique

A fundamental failure of traditional beauty education is the treatment of law, regulation, and professional rights as secondary concerns subordinate to technical skills. Students graduate from accredited cosmetology programs knowing how to cut hair, apply color, perform facials, and shape nails — but often without adequate understanding of: what a state board inspector may and may not do during an unannounced visit; what written findings they are entitled to receive; how to respond to a complaint; how to document sanitation procedures; how to appeal a disciplinary action; or how to protect their license during a dispute with an employer or a client.

NACCAS itself asks accredited schools during evaluation: “Is State Law taught as part of the curriculum? Are state board preparation classes part of the structured curriculum?” The intended answer is yes. Yet in practice, state law and regulatory procedure are often covered superficially, crowded out by the technical hours that dominate most curricula.[^22]

7.2 The Case for Integrated Compliance Education

Louisville Beauty Academy has pioneered a model of integrated compliance education grounded in the principle that a licensed beauty professional needs to understand not only how to perform their craft but how to operate lawfully, document properly, respond professionally to regulatory authority, and protect their license with the same discipline they bring to their professional skills. This model — reflected in LBA’s public education and law library, which publishes Kentucky beauty law verbatim and in plain language — treats legal knowledge as a professional competency, not an afterthought.[70][71][^60]

Di Tran University extends this model to the workforce development and continuing education context, offering structured learning on vocational integrity, compliance documentation, administrative law awareness, and institutional transparency for beauty and healthcare professionals at all career stages. The underlying philosophy, articulated clearly in LBA’s mission, is that empowered professionals — who understand their rights and obligations — are simultaneously better protected from regulatory overreach, more compliant with legitimate regulatory requirements, and better advocates for their clients and students.[72][73][^74]

7.3 What a Complete Beauty Curriculum Should Teach

A modern, ethically grounded beauty curriculum should include five categories of knowledge in addition to technical skills:

Category 1: Sanitation and Public Safety Science

- Microbiology of bacteria, viruses, and fungi relevant to beauty services

- Disinfection protocols for implements, equipment, and workstations

- Chemical safety, SDS sheets, OSHA hazard communication

- Blood-borne pathogen standards

- State-specific sanitation rules with practical application

Category 2: Law and Regulation

- State cosmetology act — verbatim study of the licensing statute

- Administrative regulations — what they require and how they are enforced

- Inspection rights and responsibilities — what inspectors may and may not do

- Licensee documentation requirements — what must be posted, logged, retained

- Federal law relevance — Title IV, OSHA, EPA, Title VI language access

Category 3: Due Process and Rights

- Constitutional foundations — property and liberty interests in licenses

- Administrative procedure — notice, hearing, response, appeal

- Open records — how to access inspection notes, complaint files, meeting minutes

- Disciplinary process step-by-step — from complaint through judicial review

- Language access rights — what interpreters and translated documents you may request

Category 4: Business Ethics and Documentation

- Written records as legal protection

- Documentation of services, consent, and adverse reactions

- Employer-employee rights in salon settings

- Consumer complaint handling and professional response

- Ethics of advertising, pricing, and client relations

Category 5: Student Rights and Institutional Accountability

- Enrollment agreements — what they require schools to do

- Student complaint processes — escalation from school to board to NACCAS to DOE

- Satisfactory academic progress and what it means for financial aid

- Transfer of hours — state requirements and limitations

- Rights upon school closure — teach-out plans and record preservation

Part VIII: Due Process Checklist for Every Beauty Professional

This checklist is intended for every licensed cosmetologist, nail technician, esthetician, shampoo technician, instructor, salon owner, and beauty school — whether in Kentucky, Tennessee, or any state. It translates constitutional and administrative law principles into practical, plain-language action steps.

SECTION A: Your Rights During an Inspection

Before the Inspector Arrives

- Keep all licenses posted and visible at all required locations

- Maintain current disinfection logs, product SDS binders, and service records

- Know the name, phone number, and email of your state board and a knowledgeable legal contact

- Display all required signage including sanitation rules where required by state law[^75]

When an Inspector Arrives

- Verify identity: Politely ask to see the inspector’s official identification and credentials

- Confirm authority: You may take reasonable time (30–60 minutes in Kentucky) to confirm records or seek clarification before signing any document[^60]

- Remain calm and professional: An inspector performing a lawful inspection has the legal right to enter; cooperation is both legally required and strategically wise

- Take notes or photographs: Document what the inspector observes, what they say, and the time and date of the inspection

- Ask for a correction notice vs. a citation: If the inspector identifies a problem, ask: “Is this a correction notice?” If yes, fix it immediately, photograph the fix, and submit written proof to the board[^45]

- Do not sign anything without reading it: Request time to read all written documents; you have the right to understand what you are signing

- Request written findings: Ask for a written inspection report before the inspector leaves; you are entitled to documentation of what was found

After the Inspection

- Write your own contemporaneous account of the inspection while memory is fresh

- Retain all inspection documentation in a permanent file

- If citations are issued, note all deadlines for response and correction

- If you disagree with any finding, do not ignore it — the deadline to respond will pass

SECTION B: Your Rights When a Complaint Is Filed Against You

- You have the right to written notice of the specific complaint and the specific rule alleged to have been violated — board cannot take adverse action without this notice

- You have the right to see the factual basis of the complaint — what was alleged, when, and by whom (where permitted under public records law)

- You have the right to respond in writing within the deadline stated in the notice — this deadline is critical and missing it can waive your right to contest the allegations

- You have the right to gather and present evidence: collect documents, photographs, service records, witness statements, and any other evidence supporting your position

- You have the right to legal representation: you may hire an attorney at any stage of the process; administrative hearings are formal proceedings and legal help is not a luxury

- Request an interpreter or translated documents if needed: under Title VI and state language access laws, if you have limited English proficiency, you may request language assistance from a government agency receiving federal funding[76][41]

- Use open records laws: submit an open records request to obtain the original inspector’s notes, complaint file, and any board communications about your case before any hearing[65][45]

SECTION C: Your Rights in a Disciplinary Hearing

- Right to adequate notice: at least 30 days’ written notice of the hearing date, time, location, and charges in most states[^62]

- Right to an impartial hearing officer: if you believe the decision-maker has a conflict of interest or bias, raise this objection in writing before the hearing

- Right to present witnesses and evidence: you may call witnesses, submit documents, and present your case fully

- Right to cross-examine adverse witnesses: the agency must afford you a meaningful opportunity to challenge the evidence against you

- Right to a written decision: the board must issue a written decision based on findings of fact and legal conclusions[64][62]

- Burden of proof: in most states, the burden is on the board to prove violations by a preponderance of the evidence[^77]

- Right to appeal: the board’s decision may be appealed to a state court — in Tennessee, to the Chancery Court of Davidson County within 60 days of the final order; in other states, timelines and procedures vary[59][62]

SECTION D: Your Rights as a Student in a Beauty School

- Enrollment agreement rights: your enrollment agreement must state the total hours, the cost, the refund policy, and the rights and obligations of both you and the school[^78]

- Right to a copy of the school catalog: you are entitled to receive a copy of the school catalog and any updates before enrollment[^79]

- Right to know about licensure requirements: the school must inform you of all state licensure requirements prior to enrollment[^22]

- Hour tracking rights: your hours must be tracked and documented accurately; you have the right to request your own hour records

- Complaint rights: if you have a complaint against your school, the process is: (1) written complaint to school administration; (2) complaint to state board; (3) complaint to NACCAS; (4) complaint to Department of Education[^69]

- Transfer rights: schools must have a written policy on accepting transfer hours; you have the right to know this policy before enrolling

- Financial aid rights: if you receive Title IV aid, you have rights to appeal financial aid decisions including satisfactory academic progress (SAP) determinations[^19]

- Record rights: upon graduation or withdrawal, you are entitled to your academic records, including your official hour transcript

SECTION E: Protecting Your School or Salon as an Owner

- Document everything in writing: all communications with the board, inspectors, students, employees, and clients should be in writing or confirmed in writing after oral discussions

- Maintain a compliance calendar: license renewal dates, inspection schedules, continuing education deadlines, accreditation report due dates, Title IV recertification dates

- Post all required notices: state law, sanitation rules, establishment license, individual licenses — inspect your postings before any inspector does[^80]

- Have a compliance contact: know the name and number of your state board contact, your accreditor’s contact, and a licensed attorney who handles professional licensing matters

- Know your inspection rights and those of your staff: train all staff on what an inspector may observe and what they should say and not say

- Build open records knowledge: know how to make and respond to open records requests in your state

- Attend board meetings: state cosmetology board meetings are public; you have the right to observe, and in many cases, to comment on proposed rule changes during notice-and-comment periods[^45]

- Participate in the rulemaking process: when the board proposes new regulations, submit written comments; you have a right to participate in shaping the rules that govern your profession

Part IX: Louisville Beauty Academy and Di Tran University as Centers of Excellence

9.1 The Institutional Philosophy

Louisville Beauty Academy (LBA) operates from a foundational principle that beauty education is incomplete without law education, compliance education, and rights education. Located in Louisville, Kentucky — a city with a significant immigrant population and a thriving Vietnamese-American community — LBA has built its institutional identity around empowering underserved populations: immigrants, refugees, single parents, and adult learners seeking meaningful career pathways. LBA’s Gold Standard of Compliance Education integrates Kentucky statutes, administrative regulations, and due process principles directly into student-facing curriculum and institutional operations.[73][70][72][60]

LBA’s commitment to multilingual outreach, flexible scheduling, and public education — including the publication of Kentucky beauty law verbatim in the LBA Public Education and Law Library — reflects a recognition that the power imbalance between regulatory authorities and ordinary licensees is best corrected not by antagonism toward regulation, but by informed, confident, documented professionalism.[71][60]

9.2 Di Tran University’s Workforce and Compliance Education Mission

Di Tran University extends this institutional philosophy to the post-secondary and continuing education context, developing curriculum that addresses vocational integrity, AI-supported compliance documentation, administrative law awareness, and transparent institutional practice. Founded by Di Tran — a Vietnamese-American entrepreneur and educator whose career embodies the immigrant journey through American occupational licensing — Di Tran University positions itself at the intersection of workforce development, legal literacy, and humanized technology integration.[74][81][^82]

The institutional model both LBA and Di Tran University represent answers the central research question of this study: the appropriate response to an imperfect and sometimes exploitative regulatory system is not ignorance, fear, or resentment — it is knowledge, documentation, professional excellence, and civic participation. When beauty professionals understand their rights as clearly as they understand their techniques, they are simultaneously safer from regulatory overreach, more compliant with legitimate requirements, better advocates for themselves and their communities, and more powerful voices for policy reform.

The educational model LBA and Di Tran University have developed — integrating technical skill with law, regulation, sanitation science, documentation discipline, ethics, and due process awareness — is a model that should be adopted nationally. Beauty schools should teach their students and graduates not only how to perform a service, but why the law requires what it requires, what they are entitled to when the government takes action against them, how to document their practice for legal protection, and who to contact when they need help.

This is not teaching cynicism about government. It is teaching citizenship. It is teaching professionalism. It is teaching the kind of informed, empowered practice that makes the beauty industry safer for clients, more dignified for workers, and more legitimate in the eyes of the law.

Conclusion: Answering the Core Research Question

Is the beauty industry regulated primarily for public safety and sanitation, or has regulation also become a tool of control over workers, students, schools, immigrants, low-income communities, and non-lawyer citizens?

The honest answer, supported by the weight of historical evidence, empirical research, constitutional law, and lived experience, is: both.

The public safety foundations of beauty regulation are real and should be respected. Sanitation requirements, disinfection protocols, and baseline competency standards protect clients from infections, chemical injuries, and incompetent practice. These protections have genuine value, and every beauty professional should understand them deeply and follow them rigorously.[9][6]

But the regulatory apparatus built on top of those foundations has, over time, accumulated layers of training hour requirements, documentation burdens, inspection powers, disciplinary procedures, and administrative complexity that — particularly as applied to immigrant workers, low-income licensees, non-English speakers, and small school operators — function as instruments of control as much as instruments of protection. The research from multiple ideological perspectives — the Obama White House, the Institute for Justice, the Brookings Institution, the Federal Trade Commission, the Minneapolis Federal Reserve, and academic researchers — is unusually consistent on this point.[83][16][51][84][31][85][39][32][^30]

The path forward requires holding both truths simultaneously: defending the public protections that work while demanding the regulatory reforms that justice requires. That means fewer arbitrary training hours disconnected from safety outcomes, more accessible language support in regulatory proceedings, greater transparency in board operations and decision-making, stronger due process protections for licensees without legal representation, and beauty education that empowers professionals to navigate the regulatory world they actually inhabit.

Louisville Beauty Academy and Di Tran University have chosen this path. Their students emerge not just as skilled technicians but as informed, rights-aware, compliance-confident professionals — the kind of graduates who strengthen their communities and their profession, protect their clients with excellence, and defend their licenses with knowledge.

That is what beauty education should be.

- U.S. Const., amend. XIV (Due Process Clause)

- U.S. Const., amend. V (Fifth Amendment Due Process)

- Mathews v. Eldridge, 424 U.S. 319 (1976) — three-factor due process balancing test[55][54]

- Board of Regents v. Roth, 408 U.S. 564 (1972) — property interest in professional licenses

- North Carolina State Board of Dental Examiners v. FTC, 574 U.S. 494 (2015) — licensing boards and antitrust[^20]

- Goldfarb v. Virginia State Bar, 421 U.S. 773 (1975) — Sherman Act applies to professional services[86][87]

- Title VI of the Civil Rights Act of 1964 — language access for LEP individuals[41][76]

- Executive Order 13166 (2000) — language access requirements

- KRS Chapter 317A — Kentucky cosmetology licensing statute

- 201 KAR Chapter 12 — Kentucky administrative regulations for cosmetology[^17]

- KRS Chapter 13B — Kentucky Administrative Procedure Act

- Modernization of Cosmetics Regulation Act of 2022 (MoCRA)[^8]

- Administrative Procedure Act, 5 U.S.C. §§ 553–706[^63]

- NACCAS Rules of Practice and Procedure[88][21][^22]

- Obama White House Report on Occupational Licensing (2015)[31][30]

- Institute for Justice, Clean Cut (2025)[^32]

- Minneapolis Federal Reserve, Occupational Licensing as Barrier to Immigrants (2023)[^39]

This research report was prepared for educational, advocacy, and institutional development purposes by Louisville Beauty Academy and Di Tran University. It is intended to inform students, graduates, licensees, salon owners, instructors, school operators, policymakers, attorneys, and regulators. It does not constitute legal advice. Individuals facing specific regulatory actions should consult a licensed attorney in their state.

- The Legal Scope of Beauty Licensing in the United States: A … – By 1927, states like California began separately licensing barbers and cosmetologists, reflecting a …

- State Board of Cosmetology agency history record. – SC ArchCat – The State Board of Cosmetic Art Examiners was established in 1934 by Act No. 771, amended by Act 259…

- Archives – State Agencies – State Board of Cosmetology – An act to regulate hairdressers and cosmetologists was passed by the legislature in 1927 along with …

- [PDF] A Review of the Board of Cosmetology – Peer – The Legislature established the Board of Cosmetology in 1948 to regulate schools, salons, and indivi…

- [PDF] An Historical Review of the Cosmetology Profession – The Illinois Beauty Culture Act of 1925 is presented with a full discussion of original licensing re…

- Safety First: The Critical Importance of Sanitation and Hygiene in … – They believe that beauty professionals understand and follow proper sanitation protocols protecting …

- Laws & Regulations – Campaign for Safe Cosmetics – In the absence of meaningful federal oversight of the cosmetics industry, states have taken steps to…

- Modernization of Cosmetics Regulation Act of 2022 (MoCRA) – FDA – … Food, Drug, and Cosmetic (FD&C) Act was passed in 1938. This new law will help ensure the safety…

- Beauty & Grooming Safety: The Importance of Sanitation – Without proper sanitation practices, harmful bacteria, fungi, and viruses can easily spread. But wit…

- Regulating Beauty: The Licensing of Barbers and Beauticians in … – Few scholars have considered the history of cosmetology and barber industries together and how licen…

- [PDF] Licensing Laws: A Historical Example of the Use of Government … – While generally not Jim. Crow laws per se, the laws were used both in the South and the. North to pr…

- What was Jim Crow – Jim Crow was the name of the racial caste system which operated primarily, but not exclusively in so…

- They’ll tell you German & European immigrants gave us barber … – Barbering was one of the first skilled trades Black men mastered in America, but when licensing came…

- Board for Barbers and Cosmetology – DPOR – Virginia.gov – The Board for Barbers and Cosmetology licenses individuals and businesses that perform barbering, co…

- Law & Rules – Ohio State Cosmetology and Barber Board – School Licenses will expire January 31 of each odd year, There will be one expiration date for a sch…

- Cosmetology – The Institute for Justice – All 50 states plus Washington, D.C. require a license to work as a cosmetologist. But the requiremen…

- 201 KAR 12:060 – Inspections | State Regulations – Law.Cornell.Edu – This administrative regulation establishes inspection and health and safety requirements for all sch…

- National Accrediting Commission of Career Arts & Sciences … – REMINDER TO NACCAS ACCREDITED SCHOOLS. Your school’s email address is important to NACCAS as a part …

- Federal Financial Aid — Title IV – Brighton Barber Institute – … Cosmetology programs are approved for Title IV funding. This means eligible students can access …

- North Carolina State Board of Dental Examiners v. FTC – Wikipedia – North Carolina State Board of Dental Examiners v. Federal Trade Commission, 574 US 494 (2015), was a…

- [PDF] NACCAS NOW – As an accredited school you have an obligation to NACCAS to continuously adhere to the Standards, Cr…

- [PDF] SAMPLE FORMS AND GUIDELINES – NACCAS – Establishes that a school participating in Title IV, HEA programs, successful course completion perc…

- Proposed Federal Rule Threatens Student Loan Access – … Title IV federal loan eligibility for most esthetics, massage therapy, and cosmetology programs …

- Cosmetology License: State-by-State Requirements, Cost & How to … – For example, California requires 3,200 apprenticeship hours compared to 1,600 school hours; Texas re…

- Are cosmetologists training longer than emergency medical … – There is no national standard on occupational licensing, so laws vary by state, but on average, cosm…

- [PDF] The State of Occupational Licensing – The report focuses on licensure requirements that affect the types of occupations studied as part of…

- Tennessee Barber License Requirements (2026) – Barber vs Cosmetologist in Tennessee: Both require 1,500 hours. The key distinction is that barbers …

- Beauty Instructor License Pathway: What to Know About Exams … – Georgia’s PSI documentation lists 750 school hours for Master Cosmetology Instructor and Hair Design…

- [PDF] Teacher Training licensing laws and requirements vary by state, as … – Cosmetologist instructor—500 classroom hours in a teacher training course and license in the individ…

- Citing Adam Smith And Milton Friedman, Obama’s Economic … – According to a new White House report, “licensing can impose substantial costs on job seekers, consu…

- White House Cites Cato in Report on Occupational Licensing – Over a quarter of U.S. workers now need licenses to do their jobs, and the percent of workers who ne…

- New Study Shows That Heavier Licensing Burdens Do Not Improve … – Institute for Justice analysis questions the necessity of expensive and time-consuming training for …

- Proposed federal student aid rule could put Atlanta beauty schools … – Programs that fail this metric in two out of three years lose access to Title IV federal financial a…

- Dept. of Education’s College Scorecard shows where student loans … – However, almost 3 percent of all graduates with student debt had degrees in Cosmetology (average ear…

- Hold cosmetology schools accountable for low earnings – At the median cosmetology school, 32 percent of students are at least three months behind on their l…

- [PDF] A STUDY OF NAIL SALON WORKERS AND INDUSTRY IN THE … – The lack of accessible languages in the curriculum training and exam process can be a barrier for so…

- [PDF] Addressing Workers Rights Violation within the Vietnamese Nail … – Nail salon workers are predominantly low-income immigrants with limited English language skills who …

- Overlooked and Unprotected – The Synergist – AIHA – The U.S. nail salon industry is predominantly owned and staffed by foreign-born individuals (immigra…

- Occupational Licensing as a Barrier to Entry for Immigrants – We find that licensure reduces foreign-born employment in a state-occupation pair by nearly 20 perce…

- [PDF] Perceived Benefits and Barriers to Implementing … – CDC Stacks – Introduction. Immigrant nail salon owners and employ- ees face multiple barriers to accessing occupa…

- Frequently Asked Questions on Legal Requirements to Provide … – “Language access” means providing Limited English Proficient (LEP) people with reasonable access to …

- Enforcement – California Board of Barbering and Cosmetology – To initiate the appeals process, a written request must be submitted. Upon receiving the appeal requ…

- USCCR Approves Report on Language Access for Individuals with … – This report surveys challenges in providing language assistance — as is required by several federal,…

- Disciplinary Actions | Barbering and Cosmetology Board – Pursuant to A.R.S. § 32-571, the Board may take any one or a combination of the following disciplina…

- Administrative Due Process & Regulatory Compliance in Kentucky … – Kentucky cosmetology law is no longer optional knowledge — it is career … examining board procedur…

- Democracy and Industry Capture of the Executive – Georgetown Law – This paper will discuss the phenomenon of regulatory capture, the threat it poses to democracy, and …

- The Case Against State Occupational Licensing Boards – Cato Institute – Licensing depresses business starts and employment, particularly among low-income and low-skilled po…

- [PDF] “Regulatory Capture”: Sources and Solutions – He is the author of REGULATING PUBLIC UTILITY PERFORMANCE: THE LAW OF MARKET STRUCTURE, PRICING AND….

- Implementing North Carolina State Board of Dental Examiners v. FTC – For the first time, the Supreme Court explicitly held that boards are not immune from federal antitr…

- Occupational Licensing Run Wild – Regulatory Transparency Project – And they often allow existing businesses … incumbent businesses endorse licensing requirements bec…

- Economic Liberty | Federal Trade Commission – Occupational licensing regulations can prevent individuals from using their vocational skills and en…

- Occupational Licensing – The Institute for Justice – Instead, they are imposed simply to protect established businesses from economic competition. IJ’s l…

- Procedural Due Process Under the Fifth Amendment – FindLaw – The Fifth Amendment states, among other things, that the government cannot deprive someone of their …

- Mathews v. Eldridge | 424 U.S. 319 (1976) – Justia Supreme Court – Mathews v. Eldridge: Procedural due process must be evaluated by using a balancing test that account…

- Amdt14.S1.5.4.2 Due Process Test in Mathews v. Eldridge – The Court concluded that due process was satisfied by a post-termination hearing with full retroacti…

- Mathews v. Eldridge – Ballotpedia – Eldridge test, for lower courts to apply when determining whether or not an individual has received …

- What is Mathews v. Eldridge test? Simple Definition & Meaning – The Mathews v. Eldridge test is a legal framework used by courts to determine what level of procedur…

- Understand Administrative Due Process and Your Legal Rights – Understand administrative due process, legal protections, and your rights. Learn how fairness, heari…

- Can I Appeal a Professional Licensing Board Decision? – If the board misapplied the law or failed to adhere to required procedures, you may appeal its decis…

- Kentucky Salon Inspection Guide: Lawful, Calm, and Professional … – Kentucky Salon Inspection Guide: Lawful, Calm, and Professional Compliance … requirements with the…

- Tennessee Administrative Procedure Act – Ballotpedia – Disciplinary and job termination proceedings for inmates under the supervision of the department (a)…

- The TN Professional Disciplinary Process – Cole Law Group – Tennessee law establishes uniform rules of procedure for hearing contested cases before state admini…

- The Lost World of the Administrative Procedure Act: A Literature … – The parties are entitled to oral arguments, rebuttal, and cross-examination of witnesses. The ALJ pr…

- Cal. Code Regs. Tit. 16, § 973.6 – Appeal Process | State Regulations – (a) A licensee that has received an immediate suspension and has been placed on probation may, withi…

- Open Record Request – Kentucky Board of Cosmetology – Kentucky Board of Cosmetology office is open from 8:00 a.m. to 4:30 p.m. EST. Please note that fees …

- Tennessee Public Records Act FAQs – The Tennessee Public Records Act provides that public records are open for inspection to any citizen…

- Open Government | Tennessee Public Records Statutes – The starting point for a discussion of the law in this area is the declaration found in T.C.A. § 10-…

- Cosmetology Degree vs. License – Let’s cut straight to the facts. California requires 1000 hours of training to qualify for a cosmeto…

- [PDF] COMPLAINT POLICY/PROCEDURE – TSPA Fargo – A complaint / grievance may be filed by any party who has good reason to believe that The Academy is…

- beauty school compliance Archives – Louisville KY – It teaches the professional environment around the service: regulation, safety, sanitation, licensin…

- Louisville Beauty Academy – A student-facing guide to Kentucky state-licensed beauty education, written with careful compliance …

- Empowering Immigrants to Build Careers and Strengthen Kentucky – Louisville Beauty Academy helps to overcome these barriers by offering accessible, high-quality educ…

- Louisville Beauty Academy Strategic Expansion Overview – Our flexible, multilingual model empowers underserved populations—immigrants, refugees, single paren…

- workforce development beauty education Archives – Di Tran University – The Gold Standard of Vocational Integrity: A Comprehensive Analysis of Transparency, Compliance, and…

- HB 1560 Update: New Requirement for Cosmetology Schools and … – The law took effect September 1, 2021, and requires all cosmetology schools and establishments to di…

- Title VI – Limited English Proficiency – TN.gov – Title VI – Limited English Proficiency. Individuals who do not speak English as their primary langua…

- Wisconsin Legislature: vol75-76 – … due process requirements under the balancing test articulated by the United States Supreme Court…

- Tennessee Cosmetology/Barber School Licenses – TN.gov – Information about getting a Cosmetology/Barber School license in Tennessee.

- Who do you call to complain about a cosmetology school? – Reddit – You could file a complaint with your state board, but most likely you will have graduated before the…

- How to Avoid Common State Board of Cosmetology Violations – Why State Board Compliance Matters · Top 10 State Board Violations (and How to Avoid Them) · What to…

- Di Tran – Founder using a live licensed school to prove AI-supported … – Founder using a live licensed school to prove AI-supported documentation, compliance readiness, mark…

- Di Tran — Founder & CEO | Visionary Leader in Workforce … – Educational institutions and trade schools pursuing humanized, AI-enabled compliance and funding mod…

- Why Professional Licensing Doesn’t Work – Vanderbilt Law School – While governments enact laws that determine which professions merit occupational licensing, regulati…

- Occupational licensing and American workers – Brookings Institution – A growing body of research suggests that licensing has pervasive impacts on workers’ wages and emplo…

- [PDF] The Multiple Justifications of Occupational Licensing – Obama White House issued a report in 2015 aimed at curtailing the use of occupational licensing it d…

- Goldfarb v. Virginia State Bar | 421 U.S. 773 (1975) – In arguing that learned professions are not “trade or commerce,” the County Bar seeks a total exclus…

- Goldfarb v. Virginia State Bar | Law | Research Starters – EBSCO – Significance: The Supreme Court promoted price competition in legal services when it held that the S…

- [PDF] NACCAS Rules of Practice & Procedure January 2017 – Persons with a direct interest in licensure or accreditation of cosmetology or massage schools and N…