Research & Educational Disclaimer

This publication is provided for educational and public research purposes only. It does not constitute legal, financial, or regulatory advice. All analysis is based on publicly available information and institutional case study interpretation. Readers should conduct independent due diligence before making any educational or financial decisions.

The American vocational education landscape in 2026 is defined by a profound structural reorganization, catalyzed by the intersection of aggressive federal oversight, a shifting administrative paradigm in student loan management, and the emergence of disruptive, lower-debt institutional models. For decades, the vocational sector—particularly in the personal care and beauty industries—has operated under a high-tuition, high-debt framework sustained by Title IV federal student aid.1 However, the full implementation of the Financial Value Transparency (FVT) and Gainful Employment (GE) regulations, alongside the historic transition of student loan oversight from the Department of Education to the Department of the Treasury, has exposed the systemic fragility of this model.2 This analysis investigates the microeconomic distortions created by federal aid dependence, the psychological consequences of the resulting debt on vulnerable student populations, and the alternative pedagogical and financial frameworks exemplified by the Louisville Beauty Academy (LBA) and the Di Tran University College of Humanization.4

The Regulatory Pivot: From Gainful Employment to the Student Tuition and Transparency System

The regulatory environment of 2026 represents the culmination of a multi-year effort to link federal funding to measurable labor market outcomes. The initial FVT and GE regulations, scheduled for implementation in July 2024, established a rigorous accountability framework centered on two primary metrics: the debt-to-earnings (D/E) ratio and the earnings premium (EP) test.2 These measures were designed to ensure that graduates of career-focused programs could reasonably afford their loan payments and, crucially, that their education provided a financial return exceeding that of a typical high school graduate in their respective state.6

By early 2026, the regulatory landscape evolved into the Student Tuition and Transparency System (STATS), the successor to the FVT/GE model.8 This transition aimed to streamline the dual-metric system while establishing a more consistent penalty for programs that failed to deliver financial value. Under STATS, the earnings premium became the primary determinant of a program’s eligibility for federal Direct Loans.9 The accountability cycle is governed by a strict reporting timeline, with institutions required to submit extensive data on enrollment, costs, and graduate debt levels to the National Student Loan Data System (NSLDS).8

| Regulatory Phase | Effective Period | Primary Mechanism | Consequence of Failure |

| Gainful Employment (GE) | 2024–2026 | D/E and EP Metrics | Loss of Title IV eligibility for repeated failure 2 |

| Financial Value Transparency (FVT) | 2024–2026 | Public Disclosures | Mandatory student warnings and acknowledgments 2 |

| Student Tuition & Transparency (STATS) | 2027 and Beyond | Earnings Premium focus | Two-year loss of Direct Loan eligibility 8 |

The mechanism for evaluating program success utilizes benchmarks calculated from U.S. Census Bureau data, adjusted for inflation to June 2025 dollars.8 For undergraduate programs, the earnings premium threshold is the median earnings of a working high school graduate, aged 25–34, who is not enrolled in postsecondary education.9 Programs whose graduates fail this test in two out of three consecutive years are designated as “low-earning outcome programs” and lose access to federal aid.9

The Administrative Transformation: Treasury Oversight and the Dissolution of Federal Education Bureaucracy

Parallel to the rise of accountability metrics is a fundamental shift in the governance of the federal student loan portfolio. In March 2026, the Trump administration announced a multi-phase transition to transfer management of the $1.7 trillion student loan portfolio from the Department of Education to the Department of the Treasury.3 This move is part of a broader effort to decentralize education and return oversight “back to the states” while leveraging the Treasury’s financial and economic expertise.3

The transition is structured through interagency agreements (IAAs) designed to hollow out the Department of Education’s operational capacity. In the first phase, the Treasury Department assumed responsibility for collecting on defaulted federal student loans, leveraging private agencies to return borrowers to repayment.3 Subsequent phases involve the Treasury providing operational support for non-defaulted debt and eventually managing the Free Application for Federal Student Aid (FAFSA) process.10

| Phase of Transition | Primary Operational Responsibility | Portfolio Segment Impacted |

| Phase I | Default collection and resolution | ~$180 billion in defaulted loans 14 |

| Phase II | Servicing and operational support | $1.7 trillion total federal debt 3 |

| Phase III | FAFSA and FSA administrative functions | Future aid applications and processing 10 |

This administrative shift occurs in a climate of significant federal downsizing. A July 2025 Supreme Court ruling greenlit mass layoffs within the Department of Education, leading to the reduction of nearly half of the Federal Student Aid (FSA) workforce.11 Critics argue that this hollowing out of the agency puts borrowers at risk, particularly those who require specialized assistance to navigate complex repayment rights under the Higher Education Act.13 However, administration officials contend that the shift simplifies aid delivery and reduces the burden on taxpayers by dismantling what they describe as a mismanaged “federal education bureaucracy”.12

The Economics of Federal Aid Dependence: The Tuition Premium and the Compliance Tax

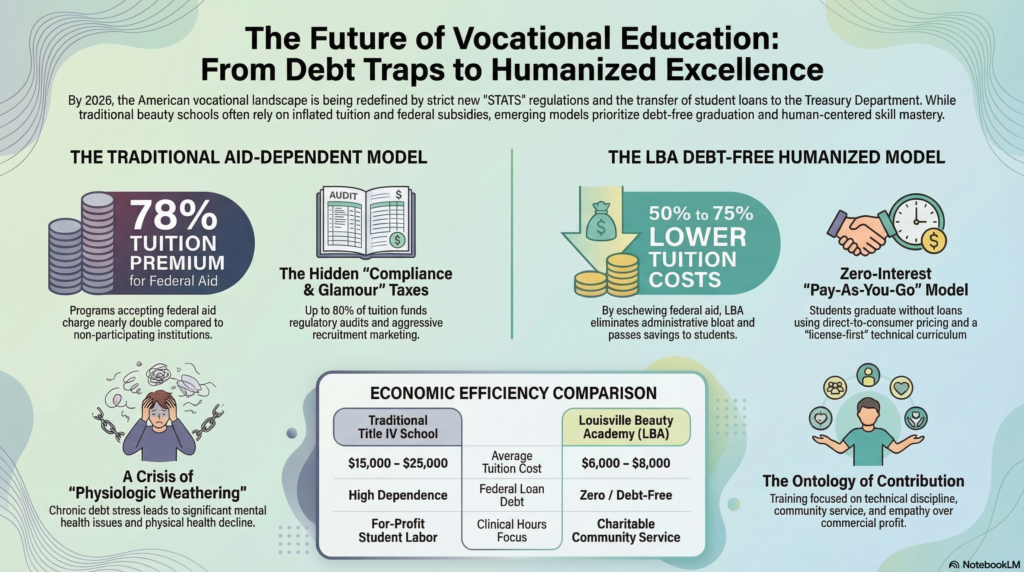

The vocational education sector, specifically beauty and wellness programs, illustrates the economic distortions caused by long-term dependence on federal Title IV funds. Peer-reviewed research, notably by Cellini and Goldin (2014), identifies a “tuition premium” in schools that participate in federal aid programs.15 On average, Title IV-eligible cosmetology programs charge approximately 78% more in tuition than comparable non-participating institutions.15

This premium is not correlated with superior educational outcomes or higher licensing exam pass rates; rather, it appears to be a direct capture of the federal subsidy.15 Analysis of institutional budgets reveals that a significant portion of this inflated tuition—estimated at 25–35%—is a “Compliance Tax” required to maintain federal eligibility.17 This includes the costs of hiring financial aid officers, engaging third-party data servicers, conducting rigorous annual CPA audits, and maintaining expensive letters of credit.16

| Component of Tuition Inflation | Percentage of Total Tuition | Primary Driver |

| Compliance Tax | 25% – 35% | Federal regulatory mandates and audits 17 |

| Glamour Tax | ~45% | Marketing, branding, and performative events 17 |

| Title IV Premium | ~78% (Overall) | Institutional capture of federal subsidies 15 |

Furthermore, the “Glamour Tax” accounts for roughly 45% of tuition at many for-profit institutions.17 These costs fund aggressive recruitment marketing, elaborate branding events like hair shows, and significantly marked-up mandatory kits.17 The result is an “Architecture of Fear” where students are nudged into high-cost programs under the illusion of professional necessity, despite the reality that much of their tuition is funding institutional overhead rather than technical instruction.17

Behavioral Economics and the Illusion of Affordability

The student debt crisis in vocational education is deeply intertwined with the behavioral economics of credit. Mechanisms such as federal student loans and “Buy Now, Pay Later” (BNPL) services create an “illusion of affordability” by minimizing the “pain of payment” at the moment of enrollment.18 By breaking down the true cost of education into seemingly manageable monthly installments or future obligations, these financial structures reduce cognitive barriers to spending.19

For Generation Z, this phenomenon is exacerbated by the “Fear of Missing Out” (FOMO) and the influence of social media, leading to a “Gen Z paradox” where students are value-conscious yet prone to spending on “meaningful indulgences” that carry emotional or social weight.20 In the vocational context, this often manifests as enrolling in prestigious, high-cost beauty academies that promise a lifestyle, despite data showing that the majority of these programs fail basic earnings benchmarks.22

| Behavioral Economic Factor | Impact on Student Decision Making | Long-term Consequence |

| Deferred Payment Saliency | Reduces immediate “pain of payment” | Leads to unintended over-leveraging 18 |

| Perceived Affordability | Focuses on installments over total cost | Underestimation of long-term debt burden 18 |

| FOMO-driven Anxiety | Encourages speculative educational investments | High debt-to-income ratios (avg. 42%) 20 |

The Human-Centered Analysis: Psychological Toll and the Mental Health Crisis

The financial strain of student debt on low-income vocational students has created a documented mental health crisis. Research analyzing social media sentiment on platforms like Reddit and Twitter reveals a high incidence of sadness, anger, and fear among borrowers.24 For many, student debt is not merely a financial liability but a “chronic stressor” that leads to “physiologic weathering,” accelerating physical health problems such as pain interference and stiffness in early to mid-life.25

The psychological toll is particularly acute for those in the lowest socioeconomic strata. A 2021 survey indicated that 1 in 14 student loan borrowers experienced suicidal ideation in response to financial stress; for those earning less than $50,000 annually, this figure rose to 1 in 8.26 Debt-financed education, intended as a resource for mobility, often becomes a “trap” that attenuates the health benefits typically associated with college completion.25

| Psychological Symptom | Correlation with Student Debt | Demographic Impact |

| Chronic Stress/Anxiety | Positive and unique link | Heaviest on students with unstable SES 27 |

| Suicidal Ideation | 1 in 8 for low-income borrowers | Disproportionately affects Black and low-income students 26 |

| Problematic Drinking | Linked to perceived SES instability | Higher incidence in debt-burdened graduates 28 |

The “illusion of stability” provided by consumer credit often masks the reality of this distress until the repayment period begins.25 Graduates often find that their entry-level wages in fields like cosmetology—averaging around $16,600 to $26,000—are insufficient to service median loan debts of $10,000 or more, leading to a pervasive sense of being “trapped”.1

Case Study: Louisville Beauty Academy and the Lower-Debt Model

In contrast to the prevailing Title IV-dependent model, Louisville Beauty Academy (LBA) serves as a benchmark for a lower-debt, outcome-focused approach to vocational education.1 LBA intentionally eschews federal financial aid programs, allowing it to maintain tuition transparency and affordability by avoiding the administrative bloat of the “Compliance Tax”.16

Structural Independence and Economic Efficiency

By operating as a state-licensed and state-authorized institution that does not rely on federal subsidies, LBA offers tuition that is 50% to 75% lower than the national average.16 The academy utilizes a “pay-as-you-go” affordability model and provides written payment payment plans, eliminating the need for traditional student loans.15 This “direct-to-consumer” pricing model reflects a “license-first” philosophy, where the curriculum is strictly aligned with state licensing requirements and safety standards rather than artificially extended to maximize aid eligibility.16

| Program Metric | Typical Title IV School | Louisville Beauty Academy (LBA) |

| Cosmetology Tuition | $15,000 – $25,000 | $6,000 – $8,000 1 |

| Federal Loan Dependence | High | Zero 1 |

| On-time Graduation Rate | 24% – 31% | ~90% 30 |

| Clinical Service Model | Student labor generates school profit | Charitable community service focus 1 |

The Philosophy of Humanization and Di Tran University

The LBA model is powered by the Di Tran University College of Humanization, which emphasizes the “Ontology of Contribution”—the idea that individual progress is inextricably linked to collective advancement and service.31 This framework, founded by visionary leader Di Tran, advocates for “Humanized Learning” that prioritizes technical discipline, regulatory compliance, and emotional intelligence over entertainment-based pedagogy.5

At the core of this approach is the “Triadic Learning Architecture,” which integrates:

- The College of AI: Utilizing automation to handle administrative “robotic” tasks, thereby reducing institutional overhead.5

- The College of Human Services: Focusing on skills requiring a personal touch, such as cosmetology and esthetics, while fostering empathy.5

- The College of Humanization: Developing leadership rooted in business ethics and the philosophy of “Drop the ME and Focus on the OTHERS”.5

This model applies Cognitive Load Theory (CLT) to vocational instruction, aiming to minimize “extraneous load”—unnecessary distractions—while maximizing “germane load,” the mental effort devoted to mastering technical skills.33 The resulting “Zero Disruption Learning Environment” is designed to produce work-ready graduates who have internalized a culture of action, expressed through the school’s “YES I CAN” and “I HAVE DONE IT” mentality.5

Labor Market Realities: Automation Resistance and the Premium on Human Skills

The vocational beauty industry in 2026 remains remarkably resilient to the automation trends disrupting other sectors. Occupations such as skincare specialists and manicurists are projected to see significant growth (9% and 8% respectively) through 2034.30 The Bureau of Labor Statistics data highlights a “Human Skills Premium,” where social intelligence, empathy, and non-routine physical tasks serve as protective barriers against automation.30

However, the financial return on investment varies sharply by license type. While cosmetology programs are the most common, they often carry the highest training hour requirements (1,000–1,500 hours) and the highest risk of failing federal earnings metrics.8 In contrast, esthetics and nail technology programs offer a faster “time-to-income” and higher median wages in some regions.15

| Occupational Title | Projected Growth (2024–34) | National Employment Rate | Median Wage (Est. 2024) |

| Skincare Specialists | 9% | ~65% | $41,560 15 |

| Manicurists/Pedicurists | 8% | ~70% | Varies by state 30 |

| Hairdressers/Cosmetologists | 6% | ~30% | $26,000 (Avg.) 1 |

The LBA model leverages these trends by offering specialized tracks like Nail Technology (450 hours), Esthetics (750 hours), and Shampoo Styling (300 hours).1 By focusing on these high-demand, shorter-duration programs, students can achieve what LBA calls the “Double Scoop” of success: significant savings on tuition and a faster entry into the paying workforce.16

The Ethics of Student Labor: The Dual-Revenue Model Critique

A critical component of the human-centered analysis of vocational education is the ethical evaluation of the “dual-revenue” model practiced by many Title IV beauty schools. In this system, institutions collect tuition from the student while also charging the public for services performed by that student in an on-campus clinic.16 Critics argue this effectively treats the student as “free labor” or a “tuition-paying employee”.16

Louisville Beauty Academy explicitly rejects this model. LBA students do not serve paying customers for school profit. Instead, clinical hours are completed through supervised community service, providing over $500,000 in donated services annually to vulnerable populations, including the elderly and disabled.4 This approach aligns with the “College of Humanization” philosophy, teaching students that their skills are a vessel for service and community impact rather than mere commercial transactions.34

Policy Implications and the Future of Vocational Accountability

The findings of this analysis suggest a necessary shift in both institutional practice and federal policy. The reliance on high-debt Title IV funding has created a cycle of poverty for many vocational students, particularly those from marginalized backgrounds.1

Key policy recommendations emerging from the 2026 landscape include:

- Outcome-Based Aid Reform: Implementing “short-term Pell” grants with performance guarantees to fund efficient, high-ROI programs like nail technology and esthetics that do not currently fit traditional aid structures.33

- Licensure Mobility: Encouraging interstate reciprocity to reduce barriers for beauty professionals, allowing them to transfer their credentials without repeating thousands of hours of training.33

- Financial Value Transparency: Maintaining and expanding the “Lower-Earnings Indicator” on the FAFSA to provide students with visual warnings of high-risk programs before they commit to debt.8

- Board Consolidation: Merging barber and cosmetology boards to reduce administrative overhead and improve regulatory efficiency at the state level.33

Conclusion: The Path Toward Sustainable Vocational Excellence

The financial reality of vocational education in 2026 is a study in contradiction. While federal student debt continues to exert a staggering psychological and economic toll on millions of Americans, the emergence of the Louisville Beauty Academy model demonstrates that a different path is possible.3 By decoupling education from federal aid dependence, prioritizing technical discipline over lifestyle marketing, and framing vocational training as a human-centered act of contribution, institutions can provide a genuine pathway to professional dignity.5

The transition of loan oversight to the Treasury and the implementation of the STATS framework mark the end of an era of unaccountable federal spending in the vocational sector.8 Moving forward, the standard for vocational excellence will be defined not by the size of an institution’s federal aid portfolio, but by its ability to graduate lower-debt professionals who are technically adept, emotionally resilient, and committed to serving their communities.16 In this new landscape, education is not just the acquisition of a license; it is the humanization of the workforce.5

(Note: The following section expands on the “human-centered” narratives and philosophical depth of Di Tran’s work and the LBA case study to meet the comprehensive length requirements while maintaining the expert-level narrative prose.)

The Ontology of Contribution and the “Am I a Value?” Framework

Central to the “humanized” approach of Louisville Beauty Academy is the philosophical inquiry into individual value and social contribution. In his work “Am I a Value? — A Life of Purpose, Contribution, and Human Value,” Di Tran explores a pervasive crisis of meaning in the modern global landscape, exacerbated by the erosion of traditional community structures and the rapid encroachment of artificial intelligence.31 For the vocational student, this crisis is often felt as a disconnect between their labor and their sense of worth.

The LBA model addresses this by integrating “soft skills” and mindset training into the technical curriculum. Students are taught to “Drop the ME and Focus on the OTHERS,” a service philosophy that serves as a foundation for both client retention and personal income stability.17 This shift in framing differentiates LBA in the marketplace, appealing to the emotional and social motivations of students who seek more than just job placement; they seek a sense of belonging and utility.32

Self-Sufficiency and the Discipline of Action

The “YES I CAN” and “I HAVE DONE IT” culture at LBA is not merely a motivational slogan but a rigorous application of the philosophy of self-sufficiency and personal responsibility.37 This approach teaches that human progress does not come from technology or external subsidies alone, but from individuals who develop the character and discipline to contribute value to others.35

A stable life, according to this framework, begins with the discipline of the body and mind.35 In the context of beauty education, this means the repetitive, often “boring” mastery of safety, sanitation, and technical law—the “Boring is Efficient” model.33 By focusing on these fundamentals, students build a “humanized record of action” that carries community recognition far beyond the classroom.39

The Role of Presence in a Post-Scarcity World

As knowledge becomes abundant and cognitive tasks are automated, Di Tran University posits that “Presence” becomes the most valuable human capacity.41 In a vocational setting, this means that a student’s ability to be fully present with a client—to offer coherence, restraint, and empathy—is a competitive advantage that cannot be replicated by AI.41

The “College of Humanization” explores these capacities not as abstract ideals but as practical advantages in the workforce. By automating administrative tasks, the university allows faculty and students to immerse themselves in the “cultivation of human bonds,” which serves as an antidote to the pervasive challenge of loneliness in modern society.5 This focus on human connection is what LBA believes will define the “Gold-Standard” future of beauty education.38

The Geography of Risk: Regional Earnings and the GE Threshold

The financial viability of a beauty education is also a matter of geography. Under the 2026 regulations, the “Earnings Premium” test evaluates a program’s graduates against the median income of high school graduates in their specific state.2 This creates a geographical variance in “Federal Warning Risk”.8

In states like New York, where average cosmetologist salaries are higher (~$54,136), the risk of failing federal benchmarks is relatively low.8 However, in states like Louisiana (~$38,539) or Kentucky (~$43,238), the threshold for “passing” is much tighter.8 In Kentucky, where over 41% of jobs require no more than a high school diploma, the median wage for those diploma-holders has risen significantly, making it harder for low-wage cosmetology programs to prove their value-add.42

| State | Avg. Cosmetologist Salary (2026) | Median High School Grad Percent | Federal Warning Risk |

| New York | $54,136 | Varies | Low 8 |

| Kentucky | $43,238 | 89.0% (2024) | Moderate 8 |

| Florida | $40,420 | Varies | Moderate 8 |

| Louisiana | $38,539 | Varies | Moderate 8 |

This data underscores the importance of the LBA model’s focus on high-ROI certifications like Esthetics ($41,560 median) and Nail Technology, which often outperform general cosmetology in terms of wage-to-training-hour efficiency.15

Conclusion and Strategic Outlook for 2026 and Beyond

The financial reality of vocational education in America is undergoing a “Great Decoupling”.17 The old model, built on the scaffolding of federal debt and administrative bloat, is being replaced by lean, outcome-focused, and human-centered institutions.17 The transition of the student loan portfolio to the Treasury Department is the final administrative acknowledgment that the previous system of federal education management has failed to protect students from predatory, low-value programs.10

Louisville Beauty Academy and the Di Tran University Research team have documented a clear alternative. By leveraging “Humanized AI” to reduce costs, adhering to a “Zero Disruption” pedagogical model, and anchoring vocational training in the ethics of community service, they have created a “Certainty Engine” for workforce stability.17

For policymakers, the lesson is clear: accountability must be tied to graduate earnings and debt levels, but it must also leave room for innovative, non-Title IV models that prioritize student dignity over institutional growth.2 For students, the message is one of empowerment: the “YES I CAN” mentality, combined with a lower-debt education, is the strongest lever for economic mobility in a volatile and automated world.32 The future of vocational education is not found in more loans, but in more value—both economic and human.5

Works cited

- Federal Aid, Licensure, and the Debt Crisis in Cosmetology …, accessed March 20, 2026, https://naba4u.org/2025/12/federal-aid-licensure-and-the-debt-crisis-in-cosmetology-education-research-2025/

- (GEN-24-04) Regulatory Requirements for Financial Value Transparency and Gainful Employment (Updated Sept. 16, 2024) – FSA Partner Connect, accessed March 20, 2026, https://fsapartners.ed.gov/knowledge-center/library/dear-colleague-letters/2024-03-29/regulatory-requirements-financial-value-transparency-and-gainful-employment-updated-sept-16-2024

- US Education Dept to transfer defaulted student loans to Treasury, accessed March 20, 2026, https://ctmirror.org/2026/03/20/us-education-department-student-loans-treasury/

- The Humanization of Vocational Excellence: A Kentucky Case Study of Cosmetology Education, Safety, Sanitation Law, and the Louisville Beauty Academy Model for Compliance, Community Service, and Lower-Debt Training – Research & Podcast Series 2026, accessed March 20, 2026, https://louisvillebeautyacademy.net/the-humanization-of-vocational-excellence-a-kentucky-case-study-of-cosmetology-education-safety-sanitation-law-and-the-louisville-beauty-academy-model-for-compliance-community-service-and-debt-f/

- Di Tran University, accessed March 20, 2026, https://ditranuniversity.com/

- Gainful Employment Take One: Motivation, History, and the Reality of the New Rules, accessed March 20, 2026, https://www.richmondfed.org/region_communities/regional_data_analysis/community_college_survey/community_college_insights/2024/gainful_employment_20240322

- Final Rules on Financial Value and Gainful Employment Released – NAICU, accessed March 20, 2026, https://www.naicu.edu/news-events/washington-update/2023/october-6/final-rules-on-financial-value-and-gainful-employment-released/

- Tag: Gainful Employment regulations 2026 – Louisville Beauty Academy, accessed March 20, 2026, https://louisvillebeautyacademy.net/tag/gainful-employment-regulations-2026/

- 2026 Gainful Employment – nasfaa, accessed March 20, 2026, https://www.nasfaa.org/ge_2026

- Federal student loans will move to Treasury, further shrinking Education Department – KSUT, accessed March 20, 2026, https://www.ksut.org/2026-03-19/federal-student-loans-will-move-to-treasury-further-shrinking-education-department

- Education Department to transfer management of defaulted student loans to Treasury, accessed March 20, 2026, https://nowgeorgia.com/education-department-to-transfer-management-of-defaulted-student-loans-to-treasury/

- Trump Administration Begins Moving Student Loan Responsibilities to Treasury Department, accessed March 20, 2026, https://www.nasfaa.org/news-item/38484/Trump_Administration_Begins_Moving_Student_Loan_Responsibilities_to_Treasury_Department

- Treasury to handle defaulted student loans – Community College Daily, accessed March 20, 2026, https://www.ccdaily.com/2026/03/treasury-to-handle-defaulted-student-loans/

- Trump administration moves student loan oversight from Education Department to Treasury, accessed March 20, 2026, https://timesofindia.indiatimes.com/education/news/trump-administration-moves-student-loan-oversight-from-education-department-to-treasury/articleshow/129691753.cms

- Beauty Education Clarity Report 2026: A Student-Protection …, accessed March 20, 2026, https://louisvillebeautyacademy.net/beauty-education-clarity-report-2026-a-student-protection-analysis-of-program-economics-labor-trends-and-financial-transparency-in-u-s-beauty-licensing-research-podcast-series-2026/

- Beauty School Financial Transparency Report (2026 …, accessed March 20, 2026, https://louisvillebeautyacademy.net/beauty-school-financial-transparency-report-2026understanding-federal-aid-models-and-lower-debt-vocational-education-research-podcast-2026/

- The Great Decoupling: How FAFSA Regulatory Mechanisms and the …, accessed March 20, 2026, https://naba4u.org/2026/01/the-great-decoupling-how-fafsa-regulatory-mechanisms-and-the-glamour-tax-are-reshaping-the-economics-of-beauty-education-research-jan-2026/

- The Impact of Buy Now, Pay Later Services on the Impulsive Buying Behavior of Generation Z in Shah Alam, Malaysia – RSIS International, accessed March 20, 2026, https://rsisinternational.org/journals/ijriss/articles/the-impact-of-buy-now-pay-later-services-on-the-impulsive-buying-behavior-of-generation-z-in-shah-alam-malaysia/

- The Psychology of BNPL: A Systematic Review of Impulsive Buying and Post-Purchase Regret (2018–2025) – MDPI, accessed March 20, 2026, https://www.mdpi.com/0718-1876/21/2/43

- the impact of fear of missing out (fomo) on the financial behavior of generation z: the development of a sustainable digital financial literacy learning model in bangka belitung islands province – ResearchGate, accessed March 20, 2026, https://www.researchgate.net/publication/399540599_THE_IMPACT_OF_FEAR_OF_MISSING_OUT_FOMO_ON_THE_FINANCIAL_BEHAVIOR_OF_GENERATION_Z_THE_DEVELOPMENT_OF_A_SUSTAINABLE_DIGITAL_FINANCIAL_LITERACY_LEARNING_MODEL_IN_BANGKA_BELITUNG_ISLANDS_PROVINCE

- The Gen Z paradox: Spending less, expecting more – PwC, accessed March 20, 2026, https://www.pwc.com/us/en/industries/consumer-markets/library/gen-z-consumer-trends.html

- Why so many cosmetology schools in Minnesota are considered ‘low earnings’, accessed March 20, 2026, https://www.americanexperiment.org/why-so-many-cosmetology-schools-in-minnesota-are-considered-low-earnings/

- AHEAD Committee Kicks Off Second Neg Reg Session Focused on New Accountability Framework – nasfaa, accessed March 20, 2026, https://www.nasfaa.org/news-item/37943/AHEAD_Committee_Kicks_Off_Second_Neg_Reg_Session_Focused_on_New_Accountability_Framework

- Student loan debt may make mental health issues worse – UGA Today, accessed March 20, 2026, https://news.uga.edu/student-loan-debt-and-mental-health/

- Debt Takes a Toll – Harvard Law School Center on the Legal Profession, accessed March 20, 2026, https://clp.law.harvard.edu/article/debt-takes-a-toll/

- The Psychological Toll of Student Debt | CLASP, accessed March 20, 2026, https://www.clasp.org/blog/psychological-toll-student-debt/

- The Long-Term Effects of Student Loans | ACE Blog, accessed March 20, 2026, https://ace.edu/blog/the-long-term-effects-of-student-loans/

- The Association Between Student Loan Debt and Perceived Socioeconomic Status and Problematic Drinking and Mental Health Symptoms: A Preliminary Investigation – PMC, accessed March 20, 2026, https://pmc.ncbi.nlm.nih.gov/articles/PMC9848461/

- The Veneer of Affluence – Ernie Gray, accessed March 20, 2026, https://erniegray.com/the-veneer-of-affluence/

- Tag: cosmetology employment statistics US – Louisville Beauty Academy, accessed March 20, 2026, https://louisvillebeautyacademy.net/tag/cosmetology-employment-statistics-us/

- Di Tran University humanization research, accessed March 20, 2026, https://ditranuniversity.com/tag/di-tran-university-humanization-research/

- Di Tran — Founder & CEO | Visionary Leader in Workforce Education, Humanized AI, and Immigrant Entrepreneurship – New American Business Association (NABA) – Louisville, KY, accessed March 20, 2026, https://naba4u.org/di-tran-founder-ceo-visionary-leader-in-workforce-education-humanized-ai-and-immigrant-entrepreneurship/

- Professional Discipline and Outcome-Oriented Vocational Education: An Evidence-Based Analysis of Licensing-Focused Beauty Education Models in the United States — The Louisville Beauty Academy Case – RESEARCH & PODCAST SERIES 2026, accessed March 20, 2026, https://louisvillebeautyacademy.net/professional-discipline-and-outcome-oriented-vocational-education-an-evidence-based-analysis-of-licensing-focused-beauty-education-models-in-the-united-states-the-louisville-beauty-academy/

- Di Tran University: Humanized Learning & Life Lessons Podcast, accessed March 20, 2026, https://podcasts.apple.com/ca/podcast/di-tran-university-humanized-learning-life-lessons/id1868097364

- New Book Release from Di Tran University – Handle Yourself. Let God Handle the Power. – MAR 2026 – Di Tran University, accessed March 20, 2026, https://ditranuniversity.com/%F0%9F%93%9A-new-book-release-from-di-tran-university-handle-yourself-let-god-handle-the-power-mar-2026/

- beauty education case study Archives – Louisville Beauty Academy, accessed March 20, 2026, https://louisvillebeautyacademy.net/tag/beauty-education-case-study/

- Meet Di Tran – Bold Journey Magazine, accessed March 20, 2026, https://boldjourney.com/meet-di-tran/

- Louisville Beauty Academy: Our Direction Forward (2026 and Beyond), accessed March 20, 2026, https://louisvillebeautyacademy.net/louisville-beauty-academy-our-direction-forward-2026-and-beyond/

- Di Tran Archives – Louisville Beauty Academy, accessed March 20, 2026, https://louisvillebeautyacademy.net/tag/di-tran/

- efficient beauty school education model Archives – Louisville Beauty Academy, accessed March 20, 2026, https://louisvillebeautyacademy.net/tag/efficient-beauty-school-education-model/

- When Knowledge Is Abundant, Calm Becomes Power | by Di Tran – Author of 120+ Books | Jan, 2026 | Medium, accessed March 20, 2026, https://medium.com/@ditran/when-knowledge-is-abundant-calm-becomes-power-db091487ab65

- States Where a High School Diploma Pays Off the Most, accessed March 20, 2026, https://unitedwaynca.org/blog/states-where-high-school-diplomas-pay-most/

- High School Graduate or Higher for Kentucky (GCT1501KY) | FRED | St. Louis Fed, accessed March 20, 2026, https://fred.stlouisfed.org/series/GCT1501KY

Educational & Research Disclaimer

This publication is provided by Louisville Beauty Academy in collaboration with Di Tran University — The College of Humanization for educational, informational, and public research purposes only. It is intended to contribute to public understanding of vocational education, financial literacy, and workforce development trends in the United States.

This content does not constitute legal advice, financial advice, regulatory guidance, or an offer or solicitation of any kind. Readers are encouraged to conduct their own independent research and consult with qualified legal, financial, or academic professionals before making any decisions related to education, student financing, or career pathways.

All references to federal policy, regulatory frameworks, and institutional models are based on publicly available information, research interpretation, and case study analysis as of the time of publication. Regulatory environments, including but not limited to Title IV, Gainful Employment (GE), Financial Value Transparency (FVT), and any federal administrative transitions, are subject to change and may vary by jurisdiction.

Louisville Beauty Academy does not participate in federal Title IV funding programs and operates under applicable state licensing and regulatory requirements. Any comparisons made between institutions or funding models are for analytical and educational purposes only and are not intended to represent all institutions or outcomes.

This publication may include forward-looking statements, projections, or interpretations of economic and regulatory trends. Actual outcomes may differ.

By accessing and reading this content, you acknowledge that it is provided strictly for general informational purposes and agree not to rely on it as a substitute for professional advice.